Business accounting activities can be tedious when performed manually and are prone to errors. For these reasons, many businesses have shifted to accounting software that offers numerous benefits, including data accuracy, time savings, easier auditing and on-demand reports.

With so many available options, it’s overwhelming to choose the right fit for a particular business. As more software vendors join the market with different enticing offers, it’s wise to be equipped with the right information.

Making a Decision Between Different Accounting Software

Each business is different and varies with industry. For efficient accounting operations, you cannot afford to choose a one-size-fits-all solution. Here are tips to help ease the selection process.

Understand your business requirements Whether you are a start-up or already have an existing business, begin by establishing your accounting requirements. This will help in making a list of features that you need in accounting software. Avoid copying other businesses without understanding what your business needs are. Consider your business size, number of users and projected growth (in order to support business scaling).

Conduct Research Learn more about accounting software options. Some might offer only general accounting features while others provide industry-specific features. By reading online reviews, you can see what users are saying about different accounting software.

Get Recommendations From Your Accountant Accountants who have already worked with the software have better knowledge about the product and can advise what will work for your business. Get their opinions.

Your Budget A business budget is a major determining factor in purchasing an accounting program. Note that software vendors have different pricing models. Depending on how much you are willing to spend, you can choose between monthly subscription fees or a pay-per-use model. Ensure that you have checked out any extra or hidden costs as you could end up spending more than initially planned. And pricing aside, avoid choosing the cheapest option just to save on expenses. The wrong software could cost your business more in the long run.

Integration with Other Software Businesses today use various software applications. It’s crucial that you select one that integrates with your existing business applications. This will help avoid duplication of work, such as manual data entry from one program to another.

Online Versus Offline Accounting Software You might prefer to have accounting software that you install on your computer, or maybe you’d rather use the online hosted version. Online accounting software is gaining popularity among SMBs due to its affordability. To use this option, you don’t need to install anything – just access it with your credentials. This allows users to access the accounting software from anywhere, even using different devices.

Availability of Customer Support Check whether the software vendor offers support after you have purchased or subscribed to use the software. What times do they offer support? And for how long will this support be available?

Data Security Data security is especially important for those who choose to work with online accounting software. Consider security measures offered by the software vendor to safeguard against data breaches and other cybersecurity risks. A good software vendor should have measures in place like automatic data backup, data encryption, and allow granular user roles to be assigned.

Parting Words

Accounting software is crucial for businesses of all sizes as it plays an important role in the accounting process; thus, you can’t afford to choose randomly. Consider all your business needs before making a choice for the best fit for your business. Create a list of preferences, then check for vendors that offer free trials to get a taste of their services before making a final decision.

Remember, choosing the right accounting software will save you from the costly mistake of replacing a wrong one.

How to Choose the Right Accounting Software for your Business

June 1, 2021 · Blog, What's New in Technology

⏱ 4 min read

Business accounting activities can be tedious when performed manually and are prone to errors. For these reasons, many businesses have shifted to accounting software that offers numerous benefits, including data accuracy, time savings, easier auditing and on-demand reports.

With so many available options, it’s overwhelming to choose the right fit for a particular business. As more software vendors join the market with different enticing offers, it’s wise to be equipped with the right information.

Making a Decision Between Different Accounting Software

Each business is different and varies with industry. For efficient accounting operations, you cannot afford to choose a one-size-fits-all solution. Here are tips to help ease the selection process.

Understand your business requirements Whether you are a start-up or already have an existing business, begin by establishing your accounting requirements. This will help in making a list of features that you need in accounting software. Avoid copying other businesses without understanding what your business needs are. Consider your business size, number of users and projected growth (in order to support business scaling).

Conduct Research Learn more about accounting software options. Some might offer only general accounting features while others provide industry-specific features. By reading online reviews, you can see what users are saying about different accounting software.

Get Recommendations From Your Accountant Accountants who have already worked with the software have better knowledge about the product and can advise what will work for your business. Get their opinions.

Your Budget A business budget is a major determining factor in purchasing an accounting program. Note that software vendors have different pricing models. Depending on how much you are willing to spend, you can choose between monthly subscription fees or a pay-per-use model. Ensure that you have checked out any extra or hidden costs as you could end up spending more than initially planned. And pricing aside, avoid choosing the cheapest option just to save on expenses. The wrong software could cost your business more in the long run.

Integration with Other Software Businesses today use various software applications. It’s crucial that you select one that integrates with your existing business applications. This will help avoid duplication of work, such as manual data entry from one program to another.

Online Versus Offline Accounting Software You might prefer to have accounting software that you install on your computer, or maybe you’d rather use the online hosted version. Online accounting software is gaining popularity among SMBs due to its affordability. To use this option, you don’t need to install anything – just access it with your credentials. This allows users to access the accounting software from anywhere, even using different devices.

Availability of Customer Support Check whether the software vendor offers support after you have purchased or subscribed to use the software. What times do they offer support? And for how long will this support be available?

Data Security Data security is especially important for those who choose to work with online accounting software. Consider security measures offered by the software vendor to safeguard against data breaches and other cybersecurity risks. A good software vendor should have measures in place like automatic data backup, data encryption, and allow granular user roles to be assigned.

Parting Words

Accounting software is crucial for businesses of all sizes as it plays an important role in the accounting process; thus, you can’t afford to choose randomly. Consider all your business needs before making a choice for the best fit for your business. Create a list of preferences, then check for vendors that offer free trials to get a taste of their services before making a final decision.

Remember, choosing the right accounting software will save you from the costly mistake of replacing a wrong one.

Disclaimer

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

Even before the pandemic began, the U.S. residential real estate market was short on houses, with more people looking to buy than those who were selling. And yet, unlike the 2008 recession, any economic woes related to the pandemic did not undercut housing prices. If anything, real estate had a banner year as home prices continued to rise. In April of this year, the median sale price of existing homes rose by 19.1 percent to a record high of $341,600.

There are several reasons we haven’t seen a repeat of the housing crisis that we experienced during the Great Recession. Today’s market is different from 2007, when the economic decline was launched by a housing bubble that sent many homeowner values underwater – followed by job losses and the inability to pay their mortgage. This time around, the government stepped in to ensure Americans didn’t lose their homes when they lost their jobs. The stimulus-relief packages included a moratorium on foreclosures and evictions. This, too, has contributed to the low inventory of existing homes, which normally would be put up for sale when owners become cash strapped.

The Homebuyers’ Market

However, in addition to the cash-strapped – we now have the cash-rich. Among the gainfully employed, savings rates increased during 2020. This means there are now several types of eager homebuyers: millennials trying to buy their first home; mid-career professionals looking to trade up; and retirees (or near-retirees) looking to make a cash offer for a smaller or second home.

The coronavirus contributed to this fiercely competitive market of buyers. Some are looking to take advantage of the newly mainstreamed remote work model and move to rural areas for a more affordable lifestyle. People who are nearing retirement are rethinking moves to large metropolitan areas or continuum of care retirement communities, where future outbreaks can spread more quickly.

The point is, there are millions of people looking to buy a home right now and not enough housing stock There are 72 million millennials alone, the oldest of who are approaching their 40s, with Generation Z right at their heels. Over the next 10 years, the demand for first-time homebuyers alone will persist regardless of how conditions change in the housing market.

The Home-Sellers’ Market

While the buyers’ market is booming with demand, the sellers’ market is starting to grow as well, just not as fast. Rising real estate values due to low inventory have presented an attractive opportunity to cash-in on home equity. In fact, according to a recent NerdWallet survey, about

17 percent of today’s homeowners say they plan to put their home on the market within the next year and a half.

The seller’s market is boosted by historically low mortgage rates, which when compared to renting make taking out a home loan even more appealing. Sellers also benefit from the near-desperation of buyers, many of whom are willing make offers before seeing the property, for as-is condition and above offer price. Not only can sellers take their pick of multiple offers, but they can often skimp on home repairs and upgrades before putting their house on the market.

In recent months, existing homes have stayed on the market for an average of only 20 days. Sellers also have the luxury of making their buyers wait under contract until the owner can buy another home. But here’s the tricky part: due to low inventory, it can be very difficult to find a replacement. Sellers who become buyers enter the fray of contract wars just like everyone else.

New Home Building

The single-family homebuilding industry recovered from last year’s economic decline quickly. In March of this year, new home starts swelled 15.3 percent to 1.238 million units. But even with the surge, real estate agents say that new builds need to range between 1.5 million and 1.6 million units per month to meet demand.

Unfortunately, one factor that is holding this market back is access to building materials. Low supply of lumber due to increased demand for new homes and renovations has catapulted lumber prices to record highs. According to the National Association of Home Builders, the cost of lumber has driven up the price of the average new single-family home by more than $35,000 within the past year.

While more inventory will come onto market as people emerge from their lockdowns and the economy fully reopens, one thing is certain: demand in the home-buying market is expected to remain high among Millennials and Gen Z for at least another decade. The momentum for high prices is expected to continue through 2021, so it may be a better time to sell than buy.

Real Estate Opportunities in 2021

June 1, 2021 · Blog, Financial Planning

⏱ 4 min read

Even before the pandemic began, the U.S. residential real estate market was short on houses, with more people looking to buy than those who were selling. And yet, unlike the 2008 recession, any economic woes related to the pandemic did not undercut housing prices. If anything, real estate had a banner year as home prices continued to rise. In April of this year, the median sale price of existing homes rose by 19.1 percent to a record high of $341,600.

There are several reasons we haven’t seen a repeat of the housing crisis that we experienced during the Great Recession. Today’s market is different from 2007, when the economic decline was launched by a housing bubble that sent many homeowner values underwater – followed by job losses and the inability to pay their mortgage. This time around, the government stepped in to ensure Americans didn’t lose their homes when they lost their jobs. The stimulus-relief packages included a moratorium on foreclosures and evictions. This, too, has contributed to the low inventory of existing homes, which normally would be put up for sale when owners become cash strapped.

The Homebuyers’ Market

However, in addition to the cash-strapped – we now have the cash-rich. Among the gainfully employed, savings rates increased during 2020. This means there are now several types of eager homebuyers: millennials trying to buy their first home; mid-career professionals looking to trade up; and retirees (or near-retirees) looking to make a cash offer for a smaller or second home.

The coronavirus contributed to this fiercely competitive market of buyers. Some are looking to take advantage of the newly mainstreamed remote work model and move to rural areas for a more affordable lifestyle. People who are nearing retirement are rethinking moves to large metropolitan areas or continuum of care retirement communities, where future outbreaks can spread more quickly.

The point is, there are millions of people looking to buy a home right now and not enough housing stock There are 72 million millennials alone, the oldest of who are approaching their 40s, with Generation Z right at their heels. Over the next 10 years, the demand for first-time homebuyers alone will persist regardless of how conditions change in the housing market.

The Home-Sellers’ Market

While the buyers’ market is booming with demand, the sellers’ market is starting to grow as well, just not as fast. Rising real estate values due to low inventory have presented an attractive opportunity to cash-in on home equity. In fact, according to a recent NerdWallet survey, about

17 percent of today’s homeowners say they plan to put their home on the market within the next year and a half.

The seller’s market is boosted by historically low mortgage rates, which when compared to renting make taking out a home loan even more appealing. Sellers also benefit from the near-desperation of buyers, many of whom are willing make offers before seeing the property, for as-is condition and above offer price. Not only can sellers take their pick of multiple offers, but they can often skimp on home repairs and upgrades before putting their house on the market.

In recent months, existing homes have stayed on the market for an average of only 20 days. Sellers also have the luxury of making their buyers wait under contract until the owner can buy another home. But here’s the tricky part: due to low inventory, it can be very difficult to find a replacement. Sellers who become buyers enter the fray of contract wars just like everyone else.

New Home Building

The single-family homebuilding industry recovered from last year’s economic decline quickly. In March of this year, new home starts swelled 15.3 percent to 1.238 million units. But even with the surge, real estate agents say that new builds need to range between 1.5 million and 1.6 million units per month to meet demand.

Unfortunately, one factor that is holding this market back is access to building materials. Low supply of lumber due to increased demand for new homes and renovations has catapulted lumber prices to record highs. According to the National Association of Home Builders, the cost of lumber has driven up the price of the average new single-family home by more than $35,000 within the past year.

While more inventory will come onto market as people emerge from their lockdowns and the economy fully reopens, one thing is certain: demand in the home-buying market is expected to remain high among Millennials and Gen Z for at least another decade. The momentum for high prices is expected to continue through 2021, so it may be a better time to sell than buy.

Disclaimer

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

President Biden presented his $1.8 trillion American Families Plan, which focuses on expanding benefits for education, children and childcare. The Biden administration intends to pay for the plan with a series of tax hikes on certain individual taxpayers. Depending on your income and source of wealth, there are some clear winners and losers of this proposal, so let’s look at each and start with those who lose.

Losers Under the Plan

High Earners: The proposed plan would increase the highest individual tax rate from 37 percent up to 39.6 percent. Currently, this tax bracket starts with those earning more than $523,000 for singles and $628,000 for taxpayers who are married filing jointly. While the percentage increase may appear small, this change is projected to raise more than $111 billion over the next 10 years.

Heirs of Large Estates: The plan proposes eliminating the “step-up” in basis on assets received when an estate is passed on. The step-up in basis means that the heir now has a basis in the inherited asset equal to the fair market value at the date of death. This essentially eliminates the payment of capital gains taxes.

The plan allows for the initial $1 million in transferred gains to remain tax-protected, so this would only impact larger estates.

Wealthy Investors: A change to the long-term capital gains and qualified dividends taxation is proposed for taxpayers earning more than $1 million per year.

Currently, long-term capital gains (on assets held for more than one year) and qualified dividends are taxed at a flat 20 percent. The plan taxes long-term capital gains and qualified dividends as ordinary income, raising the rate to 39.6 percent for the taxpayer affected.

Hedge Funds and Private Equity: The Biden plan looks to eliminate the carried interest tax break, which allows partners in the funds to treat a large portion of their compensation as long-term capital gains instead of ordinary income.

Real estate investors: Currently, the tax law allows for what are called section 1031 like-kind exchanges. A 1031 exchange allows the proceeds from the sale of real estate to be reinvested in another similar or “like-kind” asset, and defer the capital gains taxes as a result.

The proposed plan would eliminate section 1031 like-kind exchanges for all sales where there are gains of $500,000 or more.

Winners

Low and Middle-Income Families with Children: The Biden tax plan calls for a five-year extension of the expanded Child Tax Credit (CTC) created in the American Rescue Plan. The CTC gives a credit of $3,000 for every child age 6 to 17 and $3,600 for children 5 and younger for single taxpayers earning $75,000 or less and married filers earning $150,000 or less. The plan would also make the existing $2,000 CTC permanently refundable.

Low-Income Individuals Without Children: The plan proposes a permanent enlargement of the Earned Income Tax Credit. The American Rescue Plan increased the maximum benefit for filers without children from $534 to $1,502 and broadened the eligibility criteria to include those under and over 65.

Working Parents: The American Rescue Plan also included a temporary enhancement of the Child and Dependent Care Tax Credit. This credit would give qualifying families a tax credit of up to $4,000 for one child or $8,000 for more than one child to compensate for childcare costs while they work, including after-school programs. The new tax plan would make this credit permanent for those making $125,000 per year or less.

Conclusion

The benefits of the Biden tax plan for its winners are nothing new or novel. Essentially, it calls for making permanent several the provisions originally passed in the American Rescue Plan and increases taxes on wealthier taxpayers to pay for it.

The Biggest Winners and Losers in President Biden’s Proposed Individual Tax Plan

June 1, 2021 · Blog, Tax and Financial News

⏱ 3 min read

President Biden presented his $1.8 trillion American Families Plan, which focuses on expanding benefits for education, children and childcare. The Biden administration intends to pay for the plan with a series of tax hikes on certain individual taxpayers. Depending on your income and source of wealth, there are some clear winners and losers of this proposal, so let’s look at each and start with those who lose.

Losers Under the Plan

High Earners: The proposed plan would increase the highest individual tax rate from 37 percent up to 39.6 percent. Currently, this tax bracket starts with those earning more than $523,000 for singles and $628,000 for taxpayers who are married filing jointly. While the percentage increase may appear small, this change is projected to raise more than $111 billion over the next 10 years.

Heirs of Large Estates: The plan proposes eliminating the “step-up” in basis on assets received when an estate is passed on. The step-up in basis means that the heir now has a basis in the inherited asset equal to the fair market value at the date of death. This essentially eliminates the payment of capital gains taxes.

The plan allows for the initial $1 million in transferred gains to remain tax-protected, so this would only impact larger estates.

Wealthy Investors: A change to the long-term capital gains and qualified dividends taxation is proposed for taxpayers earning more than $1 million per year.

Currently, long-term capital gains (on assets held for more than one year) and qualified dividends are taxed at a flat 20 percent. The plan taxes long-term capital gains and qualified dividends as ordinary income, raising the rate to 39.6 percent for the taxpayer affected.

Hedge Funds and Private Equity: The Biden plan looks to eliminate the carried interest tax break, which allows partners in the funds to treat a large portion of their compensation as long-term capital gains instead of ordinary income.

Real estate investors: Currently, the tax law allows for what are called section 1031 like-kind exchanges. A 1031 exchange allows the proceeds from the sale of real estate to be reinvested in another similar or “like-kind” asset, and defer the capital gains taxes as a result.

The proposed plan would eliminate section 1031 like-kind exchanges for all sales where there are gains of $500,000 or more.

Winners

Low and Middle-Income Families with Children: The Biden tax plan calls for a five-year extension of the expanded Child Tax Credit (CTC) created in the American Rescue Plan. The CTC gives a credit of $3,000 for every child age 6 to 17 and $3,600 for children 5 and younger for single taxpayers earning $75,000 or less and married filers earning $150,000 or less. The plan would also make the existing $2,000 CTC permanently refundable.

Low-Income Individuals Without Children: The plan proposes a permanent enlargement of the Earned Income Tax Credit. The American Rescue Plan increased the maximum benefit for filers without children from $534 to $1,502 and broadened the eligibility criteria to include those under and over 65.

Working Parents: The American Rescue Plan also included a temporary enhancement of the Child and Dependent Care Tax Credit. This credit would give qualifying families a tax credit of up to $4,000 for one child or $8,000 for more than one child to compensate for childcare costs while they work, including after-school programs. The new tax plan would make this credit permanent for those making $125,000 per year or less.

Conclusion

The benefits of the Biden tax plan for its winners are nothing new or novel. Essentially, it calls for making permanent several the provisions originally passed in the American Rescue Plan and increases taxes on wealthier taxpayers to pay for it.

Disclaimer

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

If you’re scratching your head and wondering if we’ve lost our minds, please keep reading. You can do this. All you need to do is plan your steps – and stick to it. After all, Confucius says, “A journey of a thousand miles begins with a single step.” So let’s get moving.

Save Before You Spend

This might well be the opposite of what you do: you get your weekly or monthly paycheck, determine what expenses are ahead, then dedicate what’s left to savings. To save $10,000, the first thing to do is put away the money you’ve designated to reach your goal first (50 percent? 25 percent?), then live off the amount that’s left. Yes, it’s backwards, but in the end it’s the way forward to realize your 10k dream.

Set Up a High-Interest Savings Account

So that cash you’ve set aside? Deposit it into a savings account that will make your money grow. Several good options are Vio Bank (APY: 0.57 percent), Comenity Direct (APY: 0.55 percent), and Ally Bank (APY: 0.5 percent). This could mean the difference of hundreds (or even thousands) of dollars of interest over time.

Baby Step Your Way There

Break your goal into small chunks. Let’s say your monthly savings goal to get to 10k is $500 a month. If that’s too overwhelming, break it into two $250 chunks. If that’s too much, $125 a week, and so on. You can even parse out per day: $500 divided by 30 days in a month = $16. You can do this!

Start a Side Hustle

If you find you can’t make the amount you want to save each month and you aren’t able to tailor your expenses to fit your goal, start a side gig. For instance, if you’re able-bodied, consider helping people move and/or helping them assemble furniture. Other options include babysitting, food delivery, taking market research surveys, running errands and more. TaskRabbit is a great resource to find all kinds of ways to increase your income.

Cut Unnecessary Expenses

Look closely at your expenditures. Decide if you’re really reading that magazine and think about canceling the subscription. Pack a lunch and/or cook in for dinner. Call your internet and cell phone provider to see if they have a better deal. If you want to add an extra $1,000 to your savings each year, all you have to do is cut out $84 a month. This is doable.

Commit to a Budget

Everything that means something requires hard work and commitment. Take an afternoon, put it all down on paper, and promise to live within a dedicated financial scope. Compare your short-term gratification to your long-term financial goal. Imagine how good you’ll feel when you’ve saved $10,000. The power of visualization works.

Track Your Progress

If you’re feeling overwhelmed along the way, it pays to go back and see how far you’ve come – and we’re talking literally see it. Make your milestones visible. Hang a chart in your kitchen and color it in when you make a deposit. Or if you’re more analytical, create a spreadsheet, but keep it on your desktop. Checking this every day will help keep you on point.

Saving for a goal like this can be fun and even exciting. All you have to do is be mindful, make a conscious decision to follow your plan, and your 10k dream will be realized before your know it.

If you’re scratching your head and wondering if we’ve lost our minds, please keep reading. You can do this. All you need to do is plan your steps – and stick to it. After all, Confucius says, “A journey of a thousand miles begins with a single step.” So let’s get moving.

Save Before You Spend

This might well be the opposite of what you do: you get your weekly or monthly paycheck, determine what expenses are ahead, then dedicate what’s left to savings. To save $10,000, the first thing to do is put away the money you’ve designated to reach your goal first (50 percent? 25 percent?), then live off the amount that’s left. Yes, it’s backwards, but in the end it’s the way forward to realize your 10k dream.

Set Up a High-Interest Savings Account

So that cash you’ve set aside? Deposit it into a savings account that will make your money grow. Several good options are Vio Bank (APY: 0.57 percent), Comenity Direct (APY: 0.55 percent), and Ally Bank (APY: 0.5 percent). This could mean the difference of hundreds (or even thousands) of dollars of interest over time.

Baby Step Your Way There

Break your goal into small chunks. Let’s say your monthly savings goal to get to 10k is $500 a month. If that’s too overwhelming, break it into two $250 chunks. If that’s too much, $125 a week, and so on. You can even parse out per day: $500 divided by 30 days in a month = $16. You can do this!

Start a Side Hustle

If you find you can’t make the amount you want to save each month and you aren’t able to tailor your expenses to fit your goal, start a side gig. For instance, if you’re able-bodied, consider helping people move and/or helping them assemble furniture. Other options include babysitting, food delivery, taking market research surveys, running errands and more. TaskRabbit is a great resource to find all kinds of ways to increase your income.

Cut Unnecessary Expenses

Look closely at your expenditures. Decide if you’re really reading that magazine and think about canceling the subscription. Pack a lunch and/or cook in for dinner. Call your internet and cell phone provider to see if they have a better deal. If you want to add an extra $1,000 to your savings each year, all you have to do is cut out $84 a month. This is doable.

Commit to a Budget

Everything that means something requires hard work and commitment. Take an afternoon, put it all down on paper, and promise to live within a dedicated financial scope. Compare your short-term gratification to your long-term financial goal. Imagine how good you’ll feel when you’ve saved $10,000. The power of visualization works.

Track Your Progress

If you’re feeling overwhelmed along the way, it pays to go back and see how far you’ve come – and we’re talking literally see it. Make your milestones visible. Hang a chart in your kitchen and color it in when you make a deposit. Or if you’re more analytical, create a spreadsheet, but keep it on your desktop. Checking this every day will help keep you on point.

Saving for a goal like this can be fun and even exciting. All you have to do is be mindful, make a conscious decision to follow your plan, and your 10k dream will be realized before your know it.

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

The Child Tax Credit as we know it originated during the Clinton administration, but the recently enacted American Rescue Plan created a new version. The updated version of this tax credit could have a beneficial impact on Americans struggling through the COVID-19 pandemic. There are changes to many aspects of the credit, so let’s look at each one below.

Monthly Payments Versus Once-a-Year Credit

First, the new version of the Child Tax Credit applies only to the year 2021. If a family qualifies, the credits are $3,600 for each child under age 6 and $3,000 for those ages 6 to 17.

The major difference is not the limits, but that in 2021 half of the credit will be paid on a monthly basis in the second half of the year. From July through December, the credit will be paid out at a rate of $300 for each child under age 6 and $250 for each child ages 6 to 17. In prior years, the tax credit was available only when filing an annual tax return. The other half of the credit in 2021 will be reconciled on 2021 income tax returns.

Income Limits and Phase-Outs

Similar to the stimulus checks, the tax credit is based on adjusted gross income. To receive 100 percent of the credit, the AGI limits are $75,000 for single filers, $112,500 for heads of household and $150,000 for those married filing jointly.

The phase-outs start once a taxpayer exceeds these AGI thresholds. Every $1,000 in AGI over the limit reduces the credit by $50 (per dependent child). For example, if a couple filing jointly earned an AGI of $165,000, their credit will be reduced by $750 per child.

Qualification for the Credit

While the tax credit is ultimately based on 2021 income, to facilitate the monthly payments, the new Child Tax Credit will use 2020 income tax returns. For those who haven’t filed yet, the look-back will be to 2019. The monthly payments will be based on these already filed tax returns and then the balance of the credit be reconciled based on 2021 income.

If a taxpayer receives more interim monthly payments on the tax credit than their 2021 AGI entitles them to, they will need to pay back the unqualified portion of the credit.

Unique Situations

In the scenario where a child crosses age thresholds mid-year in 2021, the age for determining the credit will be based on how old the child is on Dec. 31, 2021. For example, a child who turns 6 before the end of the year will qualify for the lower $3,000 credit and not the $3,600 for those under 6.

Existing Child Tax Credit is Still Available

One of the unique features of the new Child Tax Credit is that the old version is still available. This version established under the Tax Cuts and Jobs Act of 2017 has significantly higher AGI thresholds: single taxpayers with an AGI of $200,000 and married filing jointly at $400,000. As a result, many taxpayers will still qualify for this version with its lower credit of $2,000 per child and no monthly payments.

Conclusion – There’s More to Come

As the July 1, 2021 start date approaches, the IRS will release more details on the new Child Tax Credit and what taxpayers can do to take advantage of the changes.

Everything There is to Know About the New Child Tax Credit

May 1, 2021 · Blog, Tax and Financial News

⏱ 3 min read

The Child Tax Credit as we know it originated during the Clinton administration, but the recently enacted American Rescue Plan created a new version. The updated version of this tax credit could have a beneficial impact on Americans struggling through the COVID-19 pandemic. There are changes to many aspects of the credit, so let’s look at each one below.

Monthly Payments Versus Once-a-Year Credit

First, the new version of the Child Tax Credit applies only to the year 2021. If a family qualifies, the credits are $3,600 for each child under age 6 and $3,000 for those ages 6 to 17.

The major difference is not the limits, but that in 2021 half of the credit will be paid on a monthly basis in the second half of the year. From July through December, the credit will be paid out at a rate of $300 for each child under age 6 and $250 for each child ages 6 to 17. In prior years, the tax credit was available only when filing an annual tax return. The other half of the credit in 2021 will be reconciled on 2021 income tax returns.

Income Limits and Phase-Outs

Similar to the stimulus checks, the tax credit is based on adjusted gross income. To receive 100 percent of the credit, the AGI limits are $75,000 for single filers, $112,500 for heads of household and $150,000 for those married filing jointly.

The phase-outs start once a taxpayer exceeds these AGI thresholds. Every $1,000 in AGI over the limit reduces the credit by $50 (per dependent child). For example, if a couple filing jointly earned an AGI of $165,000, their credit will be reduced by $750 per child.

Qualification for the Credit

While the tax credit is ultimately based on 2021 income, to facilitate the monthly payments, the new Child Tax Credit will use 2020 income tax returns. For those who haven’t filed yet, the look-back will be to 2019. The monthly payments will be based on these already filed tax returns and then the balance of the credit be reconciled based on 2021 income.

If a taxpayer receives more interim monthly payments on the tax credit than their 2021 AGI entitles them to, they will need to pay back the unqualified portion of the credit.

Unique Situations

In the scenario where a child crosses age thresholds mid-year in 2021, the age for determining the credit will be based on how old the child is on Dec. 31, 2021. For example, a child who turns 6 before the end of the year will qualify for the lower $3,000 credit and not the $3,600 for those under 6.

Existing Child Tax Credit is Still Available

One of the unique features of the new Child Tax Credit is that the old version is still available. This version established under the Tax Cuts and Jobs Act of 2017 has significantly higher AGI thresholds: single taxpayers with an AGI of $200,000 and married filing jointly at $400,000. As a result, many taxpayers will still qualify for this version with its lower credit of $2,000 per child and no monthly payments.

Conclusion – There’s More to Come

As the July 1, 2021 start date approaches, the IRS will release more details on the new Child Tax Credit and what taxpayers can do to take advantage of the changes.

Disclaimer

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

People who own a high-deductible health insurance plan may have the ability to open a health savings account (HSA). They can contribute pre-tax income to an HSA and invest the money for tax-free growth in a variety of mutual funds, stocks and exchange-traded funds (ETFs).

The funds may be withdrawn tax-free when used to pay for qualified expenses, such as the plan’s high deductible, copayments and coinsurance. The funds also can be used to purchase a wide range of health-related products.

However, a recent poll found that 40 percent of respondents who have access to a health savings account do not fully understand them. Perhaps that is why legislation passed last year that increased eligible uses of HSA funds largely went under the radar. The CARES Act included a provision that greatly expanded the number and types of health-related products and services that can be paid for with money from an HSA or an employer-sponsored Flexible Spending Account (FSA). The following list includes many of the newly eligible expenses (some require a Letter of Medical Necessity (LMN) from a licensed provider):

Over-the-counter medications, such as for fever, cold and flu, headache, muscle aches, acid, heartburn and indigestion relief, allergy and sinus relief, anti-diarrheal and constipation medicine

Toothache relief

Skin and rash ointments, medicated body lotions

Rubbing alcohol

Thermometers

Band-Aids and bandages

Kinesiology tape

Hot and cold therapy packs, cooling headache pads

Eye drops

Facial cleansers, face wipes

Prescription acne medication and over-the-counter acne treatments

Sunscreen and SPF moisturizers (including expensive anti-aging facial lotions with SPF protection)

Lip balm for sun protection and chapped lips

Sleep and snoring aids

Smoking cessation nicotine gum, patches, lozenges, inhalers and nasal sprays

Prescription sunglasses

Humidifiers, air purifiers and filters

Dietician fees

Some mental health treatments and services

Prescription hormone replacement therapy

Birth control pills

Pregnancy tests

Fertility tests

Fertility treatments such as in vitro fertilization, intrauterine insemination, fertility medication, the temporary storage of eggs or sperm

Birth classes and medically certified doulas

Breast pumps, breastfeeding classes, absorbent breast pads, breast milk storage bags

Baby monitors and potty training undies

Feminine care items, such as pads, tampons, cups and sponges

DNA/Ancestry kits

In 2021, the contribution limit for a health savings account is $3,600 for individuals and $7,200 for families; anyone age 55 or older can make an additional $1,000 annual contribution.

Just recently, the IRS published guidelines for employers regarding the use of Flexible Spending Account funds. Because of social distance guidelines and shutdowns in 2020, many people continued to work from home and contribute to their FSA but were unable to use those funds, which are generally designed to be used in the year saved (or otherwise lost).

The new guidelines allow employers to carry over or extend the grace period for unused health and/or dependent care FSA funds to the immediately following plan year. This new rule is retroactive for the 2020 and 2021 plan years. Note that while the IRS permits these new extension rules, it’s up to employers to decide what they want to do.

New Rules and Ways to Use HSAs/FSAs

May 1, 2021 · Blog, Financial Planning

⏱ 3 min read

People who own a high-deductible health insurance plan may have the ability to open a health savings account (HSA). They can contribute pre-tax income to an HSA and invest the money for tax-free growth in a variety of mutual funds, stocks and exchange-traded funds (ETFs).

The funds may be withdrawn tax-free when used to pay for qualified expenses, such as the plan’s high deductible, copayments and coinsurance. The funds also can be used to purchase a wide range of health-related products.

However, a recent poll found that 40 percent of respondents who have access to a health savings account do not fully understand them. Perhaps that is why legislation passed last year that increased eligible uses of HSA funds largely went under the radar. The CARES Act included a provision that greatly expanded the number and types of health-related products and services that can be paid for with money from an HSA or an employer-sponsored Flexible Spending Account (FSA). The following list includes many of the newly eligible expenses (some require a Letter of Medical Necessity (LMN) from a licensed provider):

Over-the-counter medications, such as for fever, cold and flu, headache, muscle aches, acid, heartburn and indigestion relief, allergy and sinus relief, anti-diarrheal and constipation medicine

Toothache relief

Skin and rash ointments, medicated body lotions

Rubbing alcohol

Thermometers

Band-Aids and bandages

Kinesiology tape

Hot and cold therapy packs, cooling headache pads

Eye drops

Facial cleansers, face wipes

Prescription acne medication and over-the-counter acne treatments

Sunscreen and SPF moisturizers (including expensive anti-aging facial lotions with SPF protection)

Lip balm for sun protection and chapped lips

Sleep and snoring aids

Smoking cessation nicotine gum, patches, lozenges, inhalers and nasal sprays

Prescription sunglasses

Humidifiers, air purifiers and filters

Dietician fees

Some mental health treatments and services

Prescription hormone replacement therapy

Birth control pills

Pregnancy tests

Fertility tests

Fertility treatments such as in vitro fertilization, intrauterine insemination, fertility medication, the temporary storage of eggs or sperm

Birth classes and medically certified doulas

Breast pumps, breastfeeding classes, absorbent breast pads, breast milk storage bags

Baby monitors and potty training undies

Feminine care items, such as pads, tampons, cups and sponges

DNA/Ancestry kits

In 2021, the contribution limit for a health savings account is $3,600 for individuals and $7,200 for families; anyone age 55 or older can make an additional $1,000 annual contribution.

Just recently, the IRS published guidelines for employers regarding the use of Flexible Spending Account funds. Because of social distance guidelines and shutdowns in 2020, many people continued to work from home and contribute to their FSA but were unable to use those funds, which are generally designed to be used in the year saved (or otherwise lost).

The new guidelines allow employers to carry over or extend the grace period for unused health and/or dependent care FSA funds to the immediately following plan year. This new rule is retroactive for the 2020 and 2021 plan years. Note that while the IRS permits these new extension rules, it’s up to employers to decide what they want to do.

Disclaimer

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

Inflation is on the rise. According to a recent Economic News Release from the U.S. Bureau of Labor Statistics (BLS), the Producer Price Index for final demand grew by 1 percent in March. February saw “final demand prices” grow by 0.5 percent; and January’s final demand prices increased by 1.3.

According to BLS, the Producer Price Index (PPI) consists of many indicators and evaluates the mean difference over a period of time for the “selling prices received by domestic producers of goods and services.” In other words, PPI is a way to gauge how much manufacturers and similar businesses face in increased costs due to inflation.

This inflation gauge takes a broad survey of approximately 10,000 unique manufactured items and the amount of inflation businesses face. The BLS’ PPI measure looks at items produced by fisheries, food growers, miners, manufacturers, etc. It also includes 72 percent of production of the service sector, as the 2007 Economic Census found.

Hedging with Futures

One way to reduce risk is by hedging. A popular example is with futures contracts. Much like buying an insurance policy, futures contracts can reduce the impact of a negative event, such as a spike in commodity prices.

If a company is worried about the price of oil for their planes or coffee for their cafes, they can enter into a futures contract to buy a designated quantity of that particular commodity at an agreed-upon price, with the ability to exercise it on or before the expiration date.

With a futures contract, a company can better plan its budget based on the contract’s parameters and the cost of the contract. If the price of the commodity rises in the future due to increased demand or limited supplies, the business can save money by taking delivery of the particular commodity at the originally agreed upon price through the futures contract.

Since the goal of hedging is to protect against losses, it’s important to weigh the cost of the futures contract. If the price of the commodity falls for the above-mentioned futures contract example, the company would still be forced to buy the commodity at the contract’s price, which would be a poor investment. If, however, it sells the futures contract before its expiration to avoid receiving the physical commodity at a poor price, that would lead to a loss. Having a contingency plan to reduce losses in futures contracts is always a good part of a hedging strategy.

Negotiate with Suppliers

Much like businesses enter into specified timeframes with suppliers, companies can do the same with their purchased supplies to provide more predictable prices. When the PPI measurement is used, the purchasing company can contract with its supplier to settle on the initial product’s price, and how price fluctuations will be determined going forward. Since the PPI is released monthly, the price can adjust accordingly (decrease or increase, depending on the PPI) for the supplier and purchasing company. It can be re-evaluated every three, six or 12 months, for example.

While there’s no predicting the future and if and how much commodity prices may rise and impact businesses, the more tools that businesses have to mitigate increased costs, the more likely they are to survive rising inflation.

Sources

https://www.bls.gov/ppi/ppifaq.htm

https://leg.mt.gov/bills/2007/fnpdf/HB0204.pdf

https://www.bls.gov/news.release/ppi.nr0.htm

How Businesses Can Hedge Against Increasing Inflation

May 1, 2021 · Blog, General Business News

⏱ 3 min read

Inflation is on the rise. According to a recent Economic News Release from the U.S. Bureau of Labor Statistics (BLS), the Producer Price Index for final demand grew by 1 percent in March. February saw “final demand prices” grow by 0.5 percent; and January’s final demand prices increased by 1.3.

According to BLS, the Producer Price Index (PPI) consists of many indicators and evaluates the mean difference over a period of time for the “selling prices received by domestic producers of goods and services.” In other words, PPI is a way to gauge how much manufacturers and similar businesses face in increased costs due to inflation.

This inflation gauge takes a broad survey of approximately 10,000 unique manufactured items and the amount of inflation businesses face. The BLS’ PPI measure looks at items produced by fisheries, food growers, miners, manufacturers, etc. It also includes 72 percent of production of the service sector, as the 2007 Economic Census found.

Hedging with Futures

One way to reduce risk is by hedging. A popular example is with futures contracts. Much like buying an insurance policy, futures contracts can reduce the impact of a negative event, such as a spike in commodity prices.

If a company is worried about the price of oil for their planes or coffee for their cafes, they can enter into a futures contract to buy a designated quantity of that particular commodity at an agreed-upon price, with the ability to exercise it on or before the expiration date.

With a futures contract, a company can better plan its budget based on the contract’s parameters and the cost of the contract. If the price of the commodity rises in the future due to increased demand or limited supplies, the business can save money by taking delivery of the particular commodity at the originally agreed upon price through the futures contract.

Since the goal of hedging is to protect against losses, it’s important to weigh the cost of the futures contract. If the price of the commodity falls for the above-mentioned futures contract example, the company would still be forced to buy the commodity at the contract’s price, which would be a poor investment. If, however, it sells the futures contract before its expiration to avoid receiving the physical commodity at a poor price, that would lead to a loss. Having a contingency plan to reduce losses in futures contracts is always a good part of a hedging strategy.

Negotiate with Suppliers

Much like businesses enter into specified timeframes with suppliers, companies can do the same with their purchased supplies to provide more predictable prices. When the PPI measurement is used, the purchasing company can contract with its supplier to settle on the initial product’s price, and how price fluctuations will be determined going forward. Since the PPI is released monthly, the price can adjust accordingly (decrease or increase, depending on the PPI) for the supplier and purchasing company. It can be re-evaluated every three, six or 12 months, for example.

While there’s no predicting the future and if and how much commodity prices may rise and impact businesses, the more tools that businesses have to mitigate increased costs, the more likely they are to survive rising inflation.

Sources

https://www.bls.gov/ppi/ppifaq.htm

https://leg.mt.gov/bills/2007/fnpdf/HB0204.pdf

https://www.bls.gov/news.release/ppi.nr0.htm

Disclaimer

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

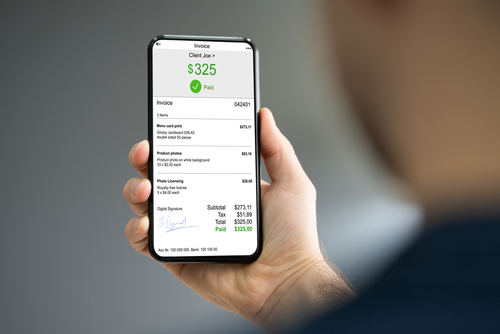

Invoicing is an important process in any business. Unfortunately, it’s also a laborious process that requires accuracy. With technology advances, businesses have tried to use various means to ease the invoicing process. Some outfits send scanned invoices; others might transfer PDFs through email; and some still use manual invoices. In this technology age, businesses are choosing to automate functions in a bid to increase overall business productivity and efficiency. E-invoicing is a technology that promises to help entrepreneurs add value to their businesses.

What is E-Invoicing?

E-invoicing is the exchange of an invoice between a buyer and seller using an integrated electronic format. This allows the buyer to pay online through a card payment, direct debit or other option after receiving the e-invoice.

E-invoicing is not a new technology; it’s already used by large scale businesses and governments. Some governments have already mandated the use of e-invoices from their suppliers and even for taxpayers. These programs have been running onsite, making it expensive for small and medium businesses (SMB) to use. Another challenge for SMBs has been dealing with multiple providers who have different platforms and technologies. This is a challenge because it requires a business to support extra business processes when sending or receiving invoices.

However, the rise of cloud computing and Software as a Service (SaaS) technologies has become an enabler for SMBs to implement e-invoicing.

Making e-invoicing available as SaaS eliminates complicated system installations and integrations that have previously been a challenge to SMBs. The SaaS systems come with features that allow you to automate the invoicing process, send reminders, accept online payments and generate reports, among other things.

Benefits of E-Invoicing

Here are some reasons that businesses are moving to e-invoicing:

Eliminates the manual process of sending invoices between a buyer and seller.

Prevents human error with the use of a template. The automated e-invoice ensures correct data is used with a validation process. This ensures there is no mistyped information, no data entry errors, no double entry, missed details or wrong data. Therefore, it improves accuracy.

Low cost of processing, since it helps to cut down on administration costs and printing invoices. It also saves a business from the task of sending emails back and forth concerning an invoice.

Maintains a more predictable cashflow as e-invoicing facilitates the seller receiving payment faster.

Enables ease of tracking invoices as you can track and trace the entire document journey. This means better accounting.

Enhanced convenience. Businesses create a different number of invoices depending on their transactions. E-invoicing provides a convenient way to store the invoices and easily retrieve them when needed.

Saves on time so you can concentrate on other business activities. There is no need to waste time looking for client information and entering data every time you need to send an invoice.

Improves the accounting process. When a business integrates e-invoicing with an accounting system, the invoicing function is faster and easier to handle.

Enhances invoice security and guaranteed delivery. There is no risk of invoices getting lost in the mail or landing in junk email. Encrypted file transfer and digital signatures are used to enhance security.

Real-time processing, which allows one to view the live delivery and processing status of an invoice.

Remote handling as SaaS can be accessed from anywhere. This makes it possible to send an invoice anytime and from anywhere as there is no need for printers or scanners.

Conclusion

The business environment is becoming increasingly competitive and the adoption of technology that automates processes can only help. E-invoicing provides an opportunity for business owners to effectively use their time on growing their business instead of spending it on a labor-intensive administration process. This service also helps SMBs align themselves with large corporations.

Finally, as with any technology, business owners should take time to research which e-invoicing service provider will best serve their unique business needs.

E-Invoicing Presents Opportunities for Businesses to Save

May 1, 2021 · Blog, What's New in Technology

⏱ 4 min read

Invoicing is an important process in any business. Unfortunately, it’s also a laborious process that requires accuracy. With technology advances, businesses have tried to use various means to ease the invoicing process. Some outfits send scanned invoices; others might transfer PDFs through email; and some still use manual invoices. In this technology age, businesses are choosing to automate functions in a bid to increase overall business productivity and efficiency. E-invoicing is a technology that promises to help entrepreneurs add value to their businesses.

What is E-Invoicing?

E-invoicing is the exchange of an invoice between a buyer and seller using an integrated electronic format. This allows the buyer to pay online through a card payment, direct debit or other option after receiving the e-invoice.

E-invoicing is not a new technology; it’s already used by large scale businesses and governments. Some governments have already mandated the use of e-invoices from their suppliers and even for taxpayers. These programs have been running onsite, making it expensive for small and medium businesses (SMB) to use. Another challenge for SMBs has been dealing with multiple providers who have different platforms and technologies. This is a challenge because it requires a business to support extra business processes when sending or receiving invoices.

However, the rise of cloud computing and Software as a Service (SaaS) technologies has become an enabler for SMBs to implement e-invoicing.

Making e-invoicing available as SaaS eliminates complicated system installations and integrations that have previously been a challenge to SMBs. The SaaS systems come with features that allow you to automate the invoicing process, send reminders, accept online payments and generate reports, among other things.

Benefits of E-Invoicing

Here are some reasons that businesses are moving to e-invoicing:

Eliminates the manual process of sending invoices between a buyer and seller.

Prevents human error with the use of a template. The automated e-invoice ensures correct data is used with a validation process. This ensures there is no mistyped information, no data entry errors, no double entry, missed details or wrong data. Therefore, it improves accuracy.

Low cost of processing, since it helps to cut down on administration costs and printing invoices. It also saves a business from the task of sending emails back and forth concerning an invoice.

Maintains a more predictable cashflow as e-invoicing facilitates the seller receiving payment faster.

Enables ease of tracking invoices as you can track and trace the entire document journey. This means better accounting.

Enhanced convenience. Businesses create a different number of invoices depending on their transactions. E-invoicing provides a convenient way to store the invoices and easily retrieve them when needed.

Saves on time so you can concentrate on other business activities. There is no need to waste time looking for client information and entering data every time you need to send an invoice.

Improves the accounting process. When a business integrates e-invoicing with an accounting system, the invoicing function is faster and easier to handle.

Enhances invoice security and guaranteed delivery. There is no risk of invoices getting lost in the mail or landing in junk email. Encrypted file transfer and digital signatures are used to enhance security.

Real-time processing, which allows one to view the live delivery and processing status of an invoice.

Remote handling as SaaS can be accessed from anywhere. This makes it possible to send an invoice anytime and from anywhere as there is no need for printers or scanners.

Conclusion

The business environment is becoming increasingly competitive and the adoption of technology that automates processes can only help. E-invoicing provides an opportunity for business owners to effectively use their time on growing their business instead of spending it on a labor-intensive administration process. This service also helps SMBs align themselves with large corporations.

Finally, as with any technology, business owners should take time to research which e-invoicing service provider will best serve their unique business needs.

Disclaimer

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

FASTER Act of 2021 (HR 578) – This bill expands the definition of major food allergens for food-labeling purposes to include sesame. It is designed to protect Americans with food allergies and related disorders that could be affected by anaphylaxis, food protein-induced enterocolitis syndrome, and eosinophilic gastrointestinal diseases. It also authorizes the Department of Health and Human Services to report on food allergy research and data collection activities. The bill was introduced by Rep. Tim Scott (R-SC) on March 3. It was passed by Congress on April 14 and is currently awaiting enactment by the president.

Advancing Education on Biosimilars Act of 2021 (S 164) – This bill was introduced by Sen. Margaret Hassan (D-NH) on Feb. 2. The legislation requires the Food and Drug Administration (FDA) to educate and promote awareness about biological products and biosimilars among healthcare providers. The FDA may also host a website to provide educational materials. This bill was passed by Congress on April 14 and is awaiting signature by the president.

TRANSPLANT Act of 2021 (HR 941) – This bill reauthorizes the Stem Cell Therapeutic and Research Act of 2005, which makes genetically matched cord blood stem cells available to patients who need them. The legislation was re-introduced by Rep. Doris Matsui (D-CA) on Feb. 8 and passed in the House on April 15. It is currently under consideration in the Senate.

504 Credit Risk Management Improvement Act of 2021 (HR 1482) – Introduced by Rep. Dan Bishop (R-NC) on March 2, this bill passed in the House on April 16 and goes to the Senate next for consideration. It amends the Small Business Act to require the administrator of the Small Business Administration to issue rules relating to environmental obligations of certified development companies and for other purposes.

504 Modernization and Small Manufacturer Enhancement Act of 2021 (HR 1490) – This bill was introduced by Rep. Angie Craig (D-MN) on March 2 and passed in the House on April 15. It is currently under consideration in the Senate. The bill would amend the Small Business Investment Act of 1958 to improve the loan guaranty program in order to enhance the ability of small manufacturers to access affordable capital. In addition, the bill adds policy goals, such as facilitating reduced costs via energy-efficient products and generating renewable energy, and providing aid to revitalize disaster areas. The bill also would increase the maximum loan amount from $5.5 million to $6.5 million for small manufacturers, and reduce the amount that they must contribute to project costs, among other provisions. The legislation authorizes each SBA district office to engage a resource partner to provide training for small manufacturers.

Fraud and Scam Reduction Act (HR 1215) – This bill would establish an office within the Federal Trade Commission and an outside advisory group for the purpose of preventing fraud that specifically targets the elderly, including mail, telephone and internet scams. Furthermore, the bill would create a Senior Scams Prevention Advisory Group to create educational materials for distribution to employees of retailers, financial services, and wire-transfer companies to help them identify and prevent scams that affect older adults. The FTC also would establish an advisory office within the Bureau of Consumer Protection to monitor scams targeting older adults, educate consumers and receive complaints. The bill was introduced by Rep. Lisa Blunt Rochester (D-DE) on Feb. 23. This bill passed in the House on April 15 and goes to the Senate next for consideration.

Advancing Healthcare Initiatives, Small Business Funding and Protecting the Elderly from Scams

May 1, 2021 · Blog, Congress at Work

⏱ 3 min read

FASTER Act of 2021 (HR 578) – This bill expands the definition of major food allergens for food-labeling purposes to include sesame. It is designed to protect Americans with food allergies and related disorders that could be affected by anaphylaxis, food protein-induced enterocolitis syndrome, and eosinophilic gastrointestinal diseases. It also authorizes the Department of Health and Human Services to report on food allergy research and data collection activities. The bill was introduced by Rep. Tim Scott (R-SC) on March 3. It was passed by Congress on April 14 and is currently awaiting enactment by the president.

Advancing Education on Biosimilars Act of 2021 (S 164) – This bill was introduced by Sen. Margaret Hassan (D-NH) on Feb. 2. The legislation requires the Food and Drug Administration (FDA) to educate and promote awareness about biological products and biosimilars among healthcare providers. The FDA may also host a website to provide educational materials. This bill was passed by Congress on April 14 and is awaiting signature by the president.

TRANSPLANT Act of 2021 (HR 941) – This bill reauthorizes the Stem Cell Therapeutic and Research Act of 2005, which makes genetically matched cord blood stem cells available to patients who need them. The legislation was re-introduced by Rep. Doris Matsui (D-CA) on Feb. 8 and passed in the House on April 15. It is currently under consideration in the Senate.

504 Credit Risk Management Improvement Act of 2021 (HR 1482) – Introduced by Rep. Dan Bishop (R-NC) on March 2, this bill passed in the House on April 16 and goes to the Senate next for consideration. It amends the Small Business Act to require the administrator of the Small Business Administration to issue rules relating to environmental obligations of certified development companies and for other purposes.

504 Modernization and Small Manufacturer Enhancement Act of 2021 (HR 1490) – This bill was introduced by Rep. Angie Craig (D-MN) on March 2 and passed in the House on April 15. It is currently under consideration in the Senate. The bill would amend the Small Business Investment Act of 1958 to improve the loan guaranty program in order to enhance the ability of small manufacturers to access affordable capital. In addition, the bill adds policy goals, such as facilitating reduced costs via energy-efficient products and generating renewable energy, and providing aid to revitalize disaster areas. The bill also would increase the maximum loan amount from $5.5 million to $6.5 million for small manufacturers, and reduce the amount that they must contribute to project costs, among other provisions. The legislation authorizes each SBA district office to engage a resource partner to provide training for small manufacturers.

Fraud and Scam Reduction Act (HR 1215) – This bill would establish an office within the Federal Trade Commission and an outside advisory group for the purpose of preventing fraud that specifically targets the elderly, including mail, telephone and internet scams. Furthermore, the bill would create a Senior Scams Prevention Advisory Group to create educational materials for distribution to employees of retailers, financial services, and wire-transfer companies to help them identify and prevent scams that affect older adults. The FTC also would establish an advisory office within the Bureau of Consumer Protection to monitor scams targeting older adults, educate consumers and receive complaints. The bill was introduced by Rep. Lisa Blunt Rochester (D-DE) on Feb. 23. This bill passed in the House on April 15 and goes to the Senate next for consideration.

Disclaimer

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

What if you could save enough for your child to go to college debt-free? It might sound impossible, but with dedication, hard work, and careful planning, you can do just that. According to Dave Ramsey, American personal finance advisor, here are the top three tax-favored plans to get started.

The Education Savings Account (ESA)

Otherwise known as the Education IRA, this plan allows you to save $2,000 (after tax) per year, per child. Let’s do that math. If you begin saving when your child is born and put away $2,000 a year until they’re 18, you’ll be investing $36,000. Not too shabby. And the good news is that qualified distributions are tax-free, which means you won’t have to pay anything when you withdraw the funds to pay for college. The other upside is, depending on the rate of growth, you’ll earn more than you would in a regular savings account. However, there are some caveats. You can’t contribute if you make more than $110,000 (single) or $220,000 (married filing jointly); the contribution cap is $2,000 a year; and the money must be used by the time your child is 30.

The 529 Plan

If you want to save more for your child’s education or you don’t qualify for the income limits of the ESA, then this might be a better fit because you can contribute up to $300,000, depending on what state you live in. Ramsey recommends you look for a 529 Plan that allows you to choose your investment funds. Also, he says most of the time there aren’t any income restrictions based on your child’s age; however, there are some limits, so choose wisely. This plan also grows tax-free. One thing to note: restrictions may apply if you want to transfer your funds to another child.

The UTMA or UGMA (Uniform Transfer/Gift to Minors Act)

One of the best things about these plans is they’re not just designed to save for education. For example, if your kiddo wants to take a gap year, this can cover living expenses. The account is set up in your child’s name but it’s controlled by a custodian (usually a parent or grandparent). The custodian manages the account until the child is 21 (18 for the UGMA). One of the pluses of this plan is that since the account is owned by the child, the earnings are usually taxed at the child’s rate, which is generally lower than that of the parents. For some people, the savings can be significant. However, there are two important things to know: (1) once your child is of legal age, she can use the funds however she likes (a trip to Europe, a sports car…or college?) and, (2) the beneficiary can’t be changed after selected.

While setting up a college fund is a smart goal, it’s not the only one. Prior to starting down these paths, Ramsey recommends that you consider paying off your mortgage, credit cards, and your own student loans. He also suggests setting up an emergency fund of three to six months and allocating 15 percent of your salary to retirement through a 401(k) and/or a Roth IRA. For more help, he recommends both parents and children read “Debt-Free Degree.” This book walks you through how to go to college without student loans.

Saving for an education might feel completely overwhelming, but if you start early enough, do your homework and create a solid plan, it’s absolutely possible.

What if you could save enough for your child to go to college debt-free? It might sound impossible, but with dedication, hard work, and careful planning, you can do just that. According to Dave Ramsey, American personal finance advisor, here are the top three tax-favored plans to get started.

The Education Savings Account (ESA)

Otherwise known as the Education IRA, this plan allows you to save $2,000 (after tax) per year, per child. Let’s do that math. If you begin saving when your child is born and put away $2,000 a year until they’re 18, you’ll be investing $36,000. Not too shabby. And the good news is that qualified distributions are tax-free, which means you won’t have to pay anything when you withdraw the funds to pay for college. The other upside is, depending on the rate of growth, you’ll earn more than you would in a regular savings account. However, there are some caveats. You can’t contribute if you make more than $110,000 (single) or $220,000 (married filing jointly); the contribution cap is $2,000 a year; and the money must be used by the time your child is 30.

The 529 Plan