Corporate profits, according to the Bureau of Economic Analysis, grew by $20.4 billion in the final quarter of 2021, a 0.7 percent increase. For the first quarter of 2022, corporate profits fell by 2.3 percent or $66.4 billion. On an annualized basis, corporate profits fell 5.2 percent in 2022, but grew 25 percent in 2021. With the economy facing inflation, the uncertainty of the Russia/Ukraine conflict, and the world working its way out of the COVID-19 pandemic, economic uncertainty abounds. For companies, measuring margins is one way to evaluate performance and strategize ways to survive and thrive in a dynamic economy. Here are a few common margins that businesses can determine to measure their financial performance.

Operating Margin Defined

Also referred to as return on sales, this measures the profit a business makes on a percentage basis, per dollar, from its core operations. It accounts for manufacturing costs that fluctuate, such as paying employees and input stock. The operating margin is determined by obtaining the business’ earnings before interest and taxes (EBIT) and dividing it by its net sales or sales revenue.

Operating Earnings = Revenue – (cost of goods sold (COGS) + overhead expenses, except tax and loan servicing costs)

Assuming a business had $10 million in revenue, $1.5 million of COGS and $750,000 in related overhead expenses, it would be as follows:

Operating Earnings = $10 million – ($1.5 million + $750,000) / $10 million

Operating Earnings = $10 million – ($2.25 million) / $10 million

Operating Earnings = $7.75 million / $10 million = 0.775 or 77.5%

Understanding the Operating Margin

This doesn’t factor in things such as taxes, interest on loans or other non-core business expenses. However, it gives a picture of what’s remaining for its non-core operating expenses, such as servicing outstanding loans. By looking at a company’s past operating margins, the trends can determine a company’s performance. Ways to improve the margin include reducing staff redundancy, negotiating better deals on raw materials or reaching more receptive customers.

Marginal Revenue Product (MRP)

If a piece of equipment or employee can create an output of X (the marginal physical product or MPP) and each additional unit of production sells at Z price (marginal revenue or MR), the MRP of the piece of the new investment is MPP x MR. Accepting that all other costs remain constant, if the business owner pays less than or equal to the MRP, it may be profitable. Otherwise, it’s not a good decision.

Using the example of a furniture manufacturer looking to respond to increased demand, this illustrates how it can guide business decisions. If a new employee can produce 100 tables every week that will retail for $100 per table, this is the MPP. Based on the calculation, the MPP of 100 multiplied by the marginal revenue (MR) of $100 = $10,000. If the business can hire and retain a new employee for less than $10,000 per week to increase their production by 100 tables per week, it can signal a positive investment.

Marginal Cost of Production

This metric is a way for businesses to determine efficient manufacturing costs. Looking at production volume, this calculation can determine if adding an additional unit to production would add profitability by examining fixed and variable costs. Fixed costs don’t change with modifications in production levels.

A static or fixed cost can be spread out over more units of increased production. However, if expanding production capacity requires additional fixed costs, it can add to the marginal cost of production, which will be explained shortly. When it comes to variable costs, as the name implies, as more production occurs, the costs similarly vary.

Assume company A makes widgets with $1 in variable costs and fixed costs of $10,000 per month, producing 5,000 widgets monthly. This would lead to $2 in fixed costs ($10,000 in fixed costs/5,000 widgets).

This final cost per widget comes to $3 ($2 fixed + $1 variable cost).

If company A chose to produce 10,000 widgets a month and they could use existing machinery, employees, etc., their fixed costs would drop to $1 ($10,000 in fixed costs/10,000 widgets).

Assuming the same variable cost of $1 per widget, plus the $1 in fixed costs, it would cost $2 per widget if the 10,000 widgets were produced. However, if additional investments (equipment, etc.) were needed to produce widget 5,001 to 10,000, this consideration would need to be factored in the marginal cost of production. If additional equipment costs $1,000 to increase production, the business would need to factor this in to see if it’s still profitable.

Essentially, if this additional production cost is less than the price of an additional individual unit, there’s the potential for a profit for the business.

Contribution Margin After Marketing (CMAM)

This measures how much cash is earned from a single unit sold after accounting for promotional and variable expenses. Example expenses include input stock, freight, inventory, etc. It’s important to distinguish between pre-planned marketing expenses over a set period of time (per month, quarter, etc.), and variable sales commissions that can fluctuate. CMAM is calculated as follows:

Looking at how much each unit can add to a business’ profitability:

CMAM for every Unit = Sales Revenue for every Unit – Variable Expenses for every Unit – Marketing Expense for every Unit

From there, a business’ net profit or loss can be found using this ratio:

Net Operating Profit = CMAM – Fixed Costs

Considerations

A smaller or negative CMAM is indicative of a product that’s likely uncompetitive. Conversely, a high CMAM, especially over a long time, can indicate the product is well regarded. It can help businesses to determine their most profitable products and/or what products to discontinue, etc.

With economic uncertainty expected to continue, keeping an eye on past, present and future margins is a key way to maintain a business’ chance of thriving in 2022 and beyond.

Corporate profits, according to the Bureau of Economic Analysis, grew by $20.4 billion in the final quarter of 2021, a 0.7 percent increase. For the first quarter of 2022, corporate profits fell by 2.3 percent or $66.4 billion. On an annualized basis, corporate profits fell 5.2 percent in 2022, but grew 25 percent in 2021. With the economy facing inflation, the uncertainty of the Russia/Ukraine conflict, and the world working its way out of the COVID-19 pandemic, economic uncertainty abounds. For companies, measuring margins is one way to evaluate performance and strategize ways to survive and thrive in a dynamic economy. Here are a few common margins that businesses can determine to measure their financial performance.

Operating Margin Defined

Also referred to as return on sales, this measures the profit a business makes on a percentage basis, per dollar, from its core operations. It accounts for manufacturing costs that fluctuate, such as paying employees and input stock. The operating margin is determined by obtaining the business’ earnings before interest and taxes (EBIT) and dividing it by its net sales or sales revenue.

Operating Earnings = Revenue – (cost of goods sold (COGS) + overhead expenses, except tax and loan servicing costs)

Assuming a business had $10 million in revenue, $1.5 million of COGS and $750,000 in related overhead expenses, it would be as follows:

Operating Earnings = $10 million – ($1.5 million + $750,000) / $10 million

Operating Earnings = $10 million – ($2.25 million) / $10 million

Operating Earnings = $7.75 million / $10 million = 0.775 or 77.5%

Understanding the Operating Margin

This doesn’t factor in things such as taxes, interest on loans or other non-core business expenses. However, it gives a picture of what’s remaining for its non-core operating expenses, such as servicing outstanding loans. By looking at a company’s past operating margins, the trends can determine a company’s performance. Ways to improve the margin include reducing staff redundancy, negotiating better deals on raw materials or reaching more receptive customers.

Marginal Revenue Product (MRP)

If a piece of equipment or employee can create an output of X (the marginal physical product or MPP) and each additional unit of production sells at Z price (marginal revenue or MR), the MRP of the piece of the new investment is MPP x MR. Accepting that all other costs remain constant, if the business owner pays less than or equal to the MRP, it may be profitable. Otherwise, it’s not a good decision.

Using the example of a furniture manufacturer looking to respond to increased demand, this illustrates how it can guide business decisions. If a new employee can produce 100 tables every week that will retail for $100 per table, this is the MPP. Based on the calculation, the MPP of 100 multiplied by the marginal revenue (MR) of $100 = $10,000. If the business can hire and retain a new employee for less than $10,000 per week to increase their production by 100 tables per week, it can signal a positive investment.

Marginal Cost of Production

This metric is a way for businesses to determine efficient manufacturing costs. Looking at production volume, this calculation can determine if adding an additional unit to production would add profitability by examining fixed and variable costs. Fixed costs don’t change with modifications in production levels.

A static or fixed cost can be spread out over more units of increased production. However, if expanding production capacity requires additional fixed costs, it can add to the marginal cost of production, which will be explained shortly. When it comes to variable costs, as the name implies, as more production occurs, the costs similarly vary.

Assume company A makes widgets with $1 in variable costs and fixed costs of $10,000 per month, producing 5,000 widgets monthly. This would lead to $2 in fixed costs ($10,000 in fixed costs/5,000 widgets).

This final cost per widget comes to $3 ($2 fixed + $1 variable cost).

If company A chose to produce 10,000 widgets a month and they could use existing machinery, employees, etc., their fixed costs would drop to $1 ($10,000 in fixed costs/10,000 widgets).

Assuming the same variable cost of $1 per widget, plus the $1 in fixed costs, it would cost $2 per widget if the 10,000 widgets were produced. However, if additional investments (equipment, etc.) were needed to produce widget 5,001 to 10,000, this consideration would need to be factored in the marginal cost of production. If additional equipment costs $1,000 to increase production, the business would need to factor this in to see if it’s still profitable.

Essentially, if this additional production cost is less than the price of an additional individual unit, there’s the potential for a profit for the business.

Contribution Margin After Marketing (CMAM)

This measures how much cash is earned from a single unit sold after accounting for promotional and variable expenses. Example expenses include input stock, freight, inventory, etc. It’s important to distinguish between pre-planned marketing expenses over a set period of time (per month, quarter, etc.), and variable sales commissions that can fluctuate. CMAM is calculated as follows:

Looking at how much each unit can add to a business’ profitability:

CMAM for every Unit = Sales Revenue for every Unit – Variable Expenses for every Unit – Marketing Expense for every Unit

From there, a business’ net profit or loss can be found using this ratio:

Net Operating Profit = CMAM – Fixed Costs

Considerations

A smaller or negative CMAM is indicative of a product that’s likely uncompetitive. Conversely, a high CMAM, especially over a long time, can indicate the product is well regarded. It can help businesses to determine their most profitable products and/or what products to discontinue, etc.

With economic uncertainty expected to continue, keeping an eye on past, present and future margins is a key way to maintain a business’ chance of thriving in 2022 and beyond.

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

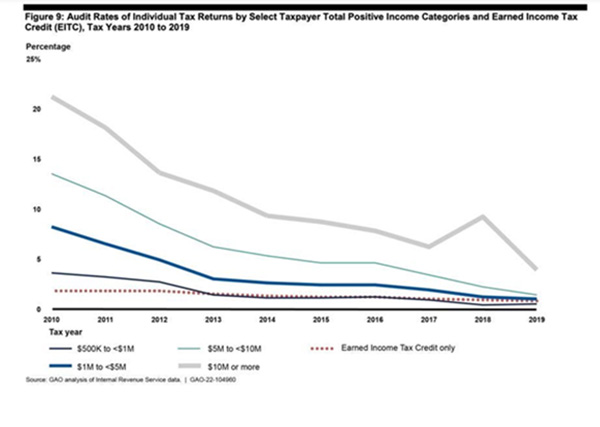

One of the perennial fears of taxpayers is getting audited by the IRS. Financially, few scenarios strike such fear into the heart of taxpayers. However, taxpayers can probably breathe a sigh of relief – at least for now. This is because the rate at which the IRS is initiating audits of individual taxpayers is dropping like a stone.

Decline in Audit Rates

The rate at which the IRS is auditing individual taxpayers has declined overall between the years of 2010 and 2019 (2020 data is too new and 2021 returns are still being filed through the extension period). According to the Government Accountability Office (GAO), nearly 1 percent of all taxpayers were audited in 2010 compared to only 0.25 percent for the tax year 2019. The GAO chart below shows the ski slope-like drop in individual tax audit rates over the period.

While the IRS continues to audit higher earning taxpayers more often overall, during the 10-year period audit rates consistently declined for all levels of taxpayers, except those with the highest incomes. The audit rate for taxpayers with income between $200k and $500k experienced the largest drop, with the audit rate declining from 2.3 percent down to 0.2 percent; a 92 percent reduction in audits. Taxpayers with the highest incomes, defined as $10 million or more, saw a resurgence in audit rates from 2017-2018; however, even they experienced an overall decline, dropping from 21.2 percent in 2019 to only 3.9 percent in 2019 – equating to an 81 percent decline.

Impact on the Treasury

There is the theory that the prospect of a tax audit leads to greater voluntary compliance. In other words, if people think they won’t get audited, then they are more likely to cheat on their taxes.

Non-compliance with tax laws and regulations have a material impact on the Treasury. According to the IRS, it is estimated that on average, individual taxpayers under-reported nearly $250 billion a year for the period 2011-2013. This obviously leads to the non-collection of taxes that are otherwise owed the government and raises issues of fairness for taxpayers who are playing by the rules.

Why the Decline in Audit Rates?

One of the main drivers is a lack of resources at the IRS, a combination of both reduced funding and less auditors on staff. The number of agents working for the IRS has declined across the board since 2011. Tax examiners, the type who handle basic audits by mail, have dropped by 18 percent. Meanwhile, revenue agents, who handle the more complex cases in the field, declined by more than 40 percent over the same period.

Demographics point to an increase in these trends as there are a wave of coming retirements in the IRS. Over the next three years, nearly 14 percent of current tax examiners and 16 percent of revenue agents are expected to retire. Stack on top of this the fact that the inexperience of newer agents and the time to complete audits is also taking longer.

Conclusion

The IRS claims it is missing out on millions in legally due tax revenues due to the inability to maintain enforcement. They say they need more funding to hire more agents to perform more audits, which not only find fraud in the audits themselves but also increase overall compliance due to the pressure this creates.

Currently, there is no political focus on bringing major new resources to the IRS, so it’s not likely to see an uptick in individual tax audit rates anytime soon. The trend of focusing on the highest earners, however, will likely continue as this is where the IRS can find the most bang for its buck.

The IRS is Auditing Fewer Returns than Ever

July 1, 2022 · Blog, Tax and Financial News

⏱ 3 min read

One of the perennial fears of taxpayers is getting audited by the IRS. Financially, few scenarios strike such fear into the heart of taxpayers. However, taxpayers can probably breathe a sigh of relief – at least for now. This is because the rate at which the IRS is initiating audits of individual taxpayers is dropping like a stone.

Decline in Audit Rates

The rate at which the IRS is auditing individual taxpayers has declined overall between the years of 2010 and 2019 (2020 data is too new and 2021 returns are still being filed through the extension period). According to the Government Accountability Office (GAO), nearly 1 percent of all taxpayers were audited in 2010 compared to only 0.25 percent for the tax year 2019. The GAO chart below shows the ski slope-like drop in individual tax audit rates over the period.

While the IRS continues to audit higher earning taxpayers more often overall, during the 10-year period audit rates consistently declined for all levels of taxpayers, except those with the highest incomes. The audit rate for taxpayers with income between $200k and $500k experienced the largest drop, with the audit rate declining from 2.3 percent down to 0.2 percent; a 92 percent reduction in audits. Taxpayers with the highest incomes, defined as $10 million or more, saw a resurgence in audit rates from 2017-2018; however, even they experienced an overall decline, dropping from 21.2 percent in 2019 to only 3.9 percent in 2019 – equating to an 81 percent decline.

Impact on the Treasury

There is the theory that the prospect of a tax audit leads to greater voluntary compliance. In other words, if people think they won’t get audited, then they are more likely to cheat on their taxes.

Non-compliance with tax laws and regulations have a material impact on the Treasury. According to the IRS, it is estimated that on average, individual taxpayers under-reported nearly $250 billion a year for the period 2011-2013. This obviously leads to the non-collection of taxes that are otherwise owed the government and raises issues of fairness for taxpayers who are playing by the rules.

Why the Decline in Audit Rates?

One of the main drivers is a lack of resources at the IRS, a combination of both reduced funding and less auditors on staff. The number of agents working for the IRS has declined across the board since 2011. Tax examiners, the type who handle basic audits by mail, have dropped by 18 percent. Meanwhile, revenue agents, who handle the more complex cases in the field, declined by more than 40 percent over the same period.

Demographics point to an increase in these trends as there are a wave of coming retirements in the IRS. Over the next three years, nearly 14 percent of current tax examiners and 16 percent of revenue agents are expected to retire. Stack on top of this the fact that the inexperience of newer agents and the time to complete audits is also taking longer.

Conclusion

The IRS claims it is missing out on millions in legally due tax revenues due to the inability to maintain enforcement. They say they need more funding to hire more agents to perform more audits, which not only find fraud in the audits themselves but also increase overall compliance due to the pressure this creates.

Currently, there is no political focus on bringing major new resources to the IRS, so it’s not likely to see an uptick in individual tax audit rates anytime soon. The trend of focusing on the highest earners, however, will likely continue as this is where the IRS can find the most bang for its buck.

Disclaimer

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

To amend the Child Nutrition Act of 1966 to establish waiver authority to address certain emergencies, disasters and supply chain disruptions, and for other purposes. (HR 7791) – In response to the recent nationwide shortage of infant formula, Congress passed a bill authorizing $28 million to fund emergency supplies and to address the potential for future shortages due to emergencies, disasters or supply chain disruptions. The bill was introduced by Rep. Jahana Hayes (D-CT) on May 17. It passed in the House on May 18 and unanimously in the Senate on May 19. It is currently awaiting signature by the president.

Ukraine Democracy Defense Lend-Lease Act of 2022 (S 3522) – This legislation was introduced on Jan. 19, by Rep. John Cornyn (T-TX). It passed in the Senate on April 6, the House on April 28, and was signed into law by President Biden on May 9. The bill waives certain requirements that constrain the president’s authority to lend or lease defense articles intended for Ukraine’s government or other Eastern European countries affected by Russia’s war. For example, prohibiting a loan or lease period of more than five years. Furthermore, the president must establish procedures to ensure quick delivery of defense articles loaned or leased to Ukraine. The provisions of this bill are scheduled to terminate at the end of FY 2023.

Additional Ukraine Supplemental Appropriations Act, 2022 (HR 7691) – Introduced by Rep. Rosa DeLauro on May 10, this bill authorizes $40.1 billion in emergency funding for U.S. agencies to aid Ukraine’s response to Russia’s invasion. The funding is available only through fiscal year 2022 (which ends Sept. 30). The appropriations are designed to provide defense equipment, migration and refugee assistance, support for nuclear power issues, emergency food assistance, economic assistance, and property seizures related to the invasion. U.S. agency recipients include the Department of Justice, the Department of Defense, the Nuclear Regulatory Commission, the Department of Health and Human Services, the Department of State, the U.S. Agency for International Development, the Department of Agriculture and the Treasury Department. The bill passed in the House and Senate on May 19 and awaits the president’s signature.

Ukraine Comprehensive Debt Payment Relief Act of 2022 (HR 7081) – This bill is designed to advocate debt assistance for Ukraine among domestic and international financial institutions. Specifically, the legislation calls for an immediate suspension of Ukraine’s debt service payments to respective institutions, offering concessional financial assistance to Ukraine, and providing economic support to both refugees from Ukraine and to the countries receiving them. The bill was introduced by Rep. Jesus Garcia (D-IL) on March 17. It passed in the House on May 11 and is under review in the Senate.

Russia and Belarus SDR Exchange Prohibition Act of 2022 (HR 6899) – The purpose of this legislation is to prevent financial assistance to Russia or Belarus. Specifically, it prohibits the U.S. Treasury Department from making transactions that involve the exchange of Special Drawing Rights held by the Russian Federation or Belarus. Special Drawing Rights (SDR) are reserve assets contributed by member countries and maintained by the International Monetary Fund (IMF). The act was introduced by Rep. French Hill (R-AK) on March 2. It passed in the House on May 11 and is in the Senate.

Isolate Russian Government Officials Act of 2022 (HR 6891) – Introduced by Rep. Ann Wagner (R-MO) on March 2, this bill is designed to exclude Russian government officials from certain international meetings, such as the Group of 20, the Basel Committee for Banking Standards, and the Bank for International Settlements. The bill’s mandate is scheduled to end either within five years, or 30 days after the president has reported (to Congress) the end of the Russian-Ukraine war. The act passed in the House on May 11; it currently resides in the Senate.

Asset Seizure for Ukraine Reconstruction Act (HR 6930) – This bill would authorize a task force to identify legal actions that can be used to confiscate the assets of foreign individuals affiliated with Russia’s political leadership. The work group also is directed to report (to Congress) its recommendations for more energy-related sanctions on Russia’s government, as well as any additional authority the president can use to seize assets. The act was introduced by Rep. Tom Malinowski (D-NJ) on March 3. It passed in the House on April 27 and is under consideration in the Senate.

Rushing Baby Formula supplies, Helping Ukraine and Punishing Russia

June 1, 2022 · Blog, Congress at Work

⏱ 4 min read

To amend the Child Nutrition Act of 1966 to establish waiver authority to address certain emergencies, disasters and supply chain disruptions, and for other purposes. (HR 7791) – In response to the recent nationwide shortage of infant formula, Congress passed a bill authorizing $28 million to fund emergency supplies and to address the potential for future shortages due to emergencies, disasters or supply chain disruptions. The bill was introduced by Rep. Jahana Hayes (D-CT) on May 17. It passed in the House on May 18 and unanimously in the Senate on May 19. It is currently awaiting signature by the president.

Ukraine Democracy Defense Lend-Lease Act of 2022 (S 3522) – This legislation was introduced on Jan. 19, by Rep. John Cornyn (T-TX). It passed in the Senate on April 6, the House on April 28, and was signed into law by President Biden on May 9. The bill waives certain requirements that constrain the president’s authority to lend or lease defense articles intended for Ukraine’s government or other Eastern European countries affected by Russia’s war. For example, prohibiting a loan or lease period of more than five years. Furthermore, the president must establish procedures to ensure quick delivery of defense articles loaned or leased to Ukraine. The provisions of this bill are scheduled to terminate at the end of FY 2023.

Additional Ukraine Supplemental Appropriations Act, 2022 (HR 7691) – Introduced by Rep. Rosa DeLauro on May 10, this bill authorizes $40.1 billion in emergency funding for U.S. agencies to aid Ukraine’s response to Russia’s invasion. The funding is available only through fiscal year 2022 (which ends Sept. 30). The appropriations are designed to provide defense equipment, migration and refugee assistance, support for nuclear power issues, emergency food assistance, economic assistance, and property seizures related to the invasion. U.S. agency recipients include the Department of Justice, the Department of Defense, the Nuclear Regulatory Commission, the Department of Health and Human Services, the Department of State, the U.S. Agency for International Development, the Department of Agriculture and the Treasury Department. The bill passed in the House and Senate on May 19 and awaits the president’s signature.

Ukraine Comprehensive Debt Payment Relief Act of 2022 (HR 7081) – This bill is designed to advocate debt assistance for Ukraine among domestic and international financial institutions. Specifically, the legislation calls for an immediate suspension of Ukraine’s debt service payments to respective institutions, offering concessional financial assistance to Ukraine, and providing economic support to both refugees from Ukraine and to the countries receiving them. The bill was introduced by Rep. Jesus Garcia (D-IL) on March 17. It passed in the House on May 11 and is under review in the Senate.

Russia and Belarus SDR Exchange Prohibition Act of 2022 (HR 6899) – The purpose of this legislation is to prevent financial assistance to Russia or Belarus. Specifically, it prohibits the U.S. Treasury Department from making transactions that involve the exchange of Special Drawing Rights held by the Russian Federation or Belarus. Special Drawing Rights (SDR) are reserve assets contributed by member countries and maintained by the International Monetary Fund (IMF). The act was introduced by Rep. French Hill (R-AK) on March 2. It passed in the House on May 11 and is in the Senate.

Isolate Russian Government Officials Act of 2022 (HR 6891) – Introduced by Rep. Ann Wagner (R-MO) on March 2, this bill is designed to exclude Russian government officials from certain international meetings, such as the Group of 20, the Basel Committee for Banking Standards, and the Bank for International Settlements. The bill’s mandate is scheduled to end either within five years, or 30 days after the president has reported (to Congress) the end of the Russian-Ukraine war. The act passed in the House on May 11; it currently resides in the Senate.

Asset Seizure for Ukraine Reconstruction Act (HR 6930) – This bill would authorize a task force to identify legal actions that can be used to confiscate the assets of foreign individuals affiliated with Russia’s political leadership. The work group also is directed to report (to Congress) its recommendations for more energy-related sanctions on Russia’s government, as well as any additional authority the president can use to seize assets. The act was introduced by Rep. Tom Malinowski (D-NJ) on March 3. It passed in the House on April 27 and is under consideration in the Senate.

Disclaimer

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

Cash flow awareness is vital in running the day-to-day activities of a business. Keeping track of the inflows and outflows helps a company make better plans and decisions, such as the right time to expand. Cash flow knowledge reveals where a business is spending money and can protect business relations, among other benefits. However, tracking cash flow is a challenge for many businesses.

To avoid business failure due to poor cash flow management, business owners are investing in software applications to help manage cash flow challenges. Modern technology enables access to these applications over the cloud, giving small- and medium-sized businesses the opportunity to benefit from them. These cash flow management tools help companies improve cash flow in various ways.

Remove Manual Paper Systems that Cost Time and Money Using a cash flow automated system, it’s possible to create and send invoices directly to clients through email. This saves on time that would otherwise be used for printing invoices, mailing, bank trips, and going through paperwork comparing details. It is also possible to automate recurring invoices, saving the time used to create and send invoices.

Makes it Easy for Clients to Pay Paying invoices takes time if a client has to keep confirming the payment details. However, an automated invoice can contain a pay now link, which facilitates quick payments for applications that include access to online payment options.

Helps Avoid Data Entry Errors and Reduces Risks There is no need to move from one platform to another to check details, manually enter details, verify figures, etc. This ensures fewer errors, such as those generated when copying details like bank information to a check, or paying the wrong amount. Sorting out these errors takes time, hence delaying payments.

Cash Flow Forecast The applications offer access to account insights in real time using cloud-based software and mobile apps, making it possible to forecast when clients are likely to pay and when bills are due. Access to live data also means there is no more dealing with complicated spreadsheets and paper ledgers. This way, a business can plan its actions to ensure positive cash flow. For instance, a business can delay paying vendors and plan when best to pay bills without running out of standby cash.

Avoid Late Payments Late payments can result in fines that will cost the business unnecessary losses. However, with software that automatically sends invoice reminders, it is possible to make timely payments.

Centralized Cash Flow System All activities involving cash transactions are located in one system, offering the ability to see cash inflows and outflows at a glance. As a result, a business can streamline its accounts and monitor cash flow; and since it includes real-time reporting, it’s easy to spot any red flags and solve problems that could adversely affect a business.

Leverage on Data Analytics A centralized system will collect data and store it in one place. By deploying artificial intelligence technology that performs data analysis, a business can better forecast its cash flow. This also provides insight into how changes such as a new products or price adjustments affect cash flow.

Choosing a Cash Flow Tool

Cash flow automation enables a business to maintain a positive cash flow and have cash in its reserves to afford reinvesting in its operations, settling debts, and handling other operating costs. However, before investing in an automation tool, it’s recommended to analyze different tools to find the best fit for your business. Each tool is different and built to address various business problems.

Some features to look out for include integration with the existing accounting system, payments and invoicing, accepting a variety of payment methods, and security.

Besides getting the most suitable application, there are other considerations to establishing a healthy cash flow. Technology has its benefits, but it does not act as a cure for a poorly implemented system. For instance, if employees don’t know how to use new technology, its impact will be limited. Therefore, a business should establish a workflow process before implementing any new technology.

Ways Technology Can Improve Business Cash Flow

June 1, 2022 · Blog, What's New in Technology

⏱ 4 min read

Cash flow awareness is vital in running the day-to-day activities of a business. Keeping track of the inflows and outflows helps a company make better plans and decisions, such as the right time to expand. Cash flow knowledge reveals where a business is spending money and can protect business relations, among other benefits. However, tracking cash flow is a challenge for many businesses.

To avoid business failure due to poor cash flow management, business owners are investing in software applications to help manage cash flow challenges. Modern technology enables access to these applications over the cloud, giving small- and medium-sized businesses the opportunity to benefit from them. These cash flow management tools help companies improve cash flow in various ways.

Remove Manual Paper Systems that Cost Time and Money Using a cash flow automated system, it’s possible to create and send invoices directly to clients through email. This saves on time that would otherwise be used for printing invoices, mailing, bank trips, and going through paperwork comparing details. It is also possible to automate recurring invoices, saving the time used to create and send invoices.

Makes it Easy for Clients to Pay Paying invoices takes time if a client has to keep confirming the payment details. However, an automated invoice can contain a pay now link, which facilitates quick payments for applications that include access to online payment options.

Helps Avoid Data Entry Errors and Reduces Risks There is no need to move from one platform to another to check details, manually enter details, verify figures, etc. This ensures fewer errors, such as those generated when copying details like bank information to a check, or paying the wrong amount. Sorting out these errors takes time, hence delaying payments.

Cash Flow Forecast The applications offer access to account insights in real time using cloud-based software and mobile apps, making it possible to forecast when clients are likely to pay and when bills are due. Access to live data also means there is no more dealing with complicated spreadsheets and paper ledgers. This way, a business can plan its actions to ensure positive cash flow. For instance, a business can delay paying vendors and plan when best to pay bills without running out of standby cash.

Avoid Late Payments Late payments can result in fines that will cost the business unnecessary losses. However, with software that automatically sends invoice reminders, it is possible to make timely payments.

Centralized Cash Flow System All activities involving cash transactions are located in one system, offering the ability to see cash inflows and outflows at a glance. As a result, a business can streamline its accounts and monitor cash flow; and since it includes real-time reporting, it’s easy to spot any red flags and solve problems that could adversely affect a business.

Leverage on Data Analytics A centralized system will collect data and store it in one place. By deploying artificial intelligence technology that performs data analysis, a business can better forecast its cash flow. This also provides insight into how changes such as a new products or price adjustments affect cash flow.

Choosing a Cash Flow Tool

Cash flow automation enables a business to maintain a positive cash flow and have cash in its reserves to afford reinvesting in its operations, settling debts, and handling other operating costs. However, before investing in an automation tool, it’s recommended to analyze different tools to find the best fit for your business. Each tool is different and built to address various business problems.

Some features to look out for include integration with the existing accounting system, payments and invoicing, accepting a variety of payment methods, and security.

Besides getting the most suitable application, there are other considerations to establishing a healthy cash flow. Technology has its benefits, but it does not act as a cure for a poorly implemented system. For instance, if employees don’t know how to use new technology, its impact will be limited. Therefore, a business should establish a workflow process before implementing any new technology.

Disclaimer

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

You love summer, don’t you? School’s out, and BBQs are on. But what you probably don’t love are those higher air conditioning bills. Here are some tried-and-true ways to help lower the cost of keeping cool.

Change Air Filters

Make sure you switch out your filters before those sizzling summer temps arrive, then once a month after that. When filters are dirty, they block the airflow, which causes your air conditioner to work harder when cooling your home. You’ll not only lower your bills by five to 15 percent, but you will also extend the life of your entire A/C system. If you don’t change those clogged filters, it could create a malfunction, and you’ll have to get your unit repaired.

Turn Up Your Thermostat

Set it to 78 degrees and shed a few layers. Yes, this might not be preferable to your icy 72 degrees, but you know what will feel good? Seeing your electricity bill go down 18 percent.

Run the Ceiling Fan

This works in tandem with turning your thermostat to 78 degrees. If you’ve been running your fan clockwise during the previous months, be sure to change the direction so the air moves down into the room.

Invest In a Smart Thermostat

With these babies, you can regulate the temps when you’re not home from an app on your phone or via voice commands. For instance, you can set the A/C to a toasty 80 degrees when you’re not home to save money. Two good brands to check into are Nest and Ecobee. They’re well worth the cost.

Close Your Curtains and Blinds

When the sun’s rays enter your home, they heat up the room and your thermostat. The best time to shut your curtains and blinds is during the warmest part of the day, between (roughly) 10 a.m. and 3 p.m. This will help insulate your windows and stop the cool air from escaping.

Consider the Placement of Your Thermostat

Where do you have this? If it’s next to a hot window, your poor A/C will work harder than it needs to because it will think the room’s hotter than it is. Other places not to put it are near doors that could let in drafts. Or by bathrooms that are usually warm and steamy. In fact, the U.S. Office of Energy Efficiency and Renewable Energy advises avoiding placing thermostats near lamps or TVs. Why? They release heat that could confuse the sensors of your poor, struggling device.

Avoid Activities that Heat Up the House

Avoid using the oven, dishwasher, or dryer during the middle of the day. This heats up the house. Instead, use the microwave, grill outside, or wash your dishes by hand if you can stand it. If you need to dry clothes, wait until after sundown.

Check Your Air-Conditioner

If you had some issues with it last summer, get someone (a professional) to take a look at it before the high temps descend upon you. If you make a few small repairs, you’ll save mightily in the long run.

If you implement one or all of these tips, you’ll be in a much better, cooler place come full-on summer, the time of year when you most want to chill.

You love summer, don’t you? School’s out, and BBQs are on. But what you probably don’t love are those higher air conditioning bills. Here are some tried-and-true ways to help lower the cost of keeping cool.

Change Air Filters

Make sure you switch out your filters before those sizzling summer temps arrive, then once a month after that. When filters are dirty, they block the airflow, which causes your air conditioner to work harder when cooling your home. You’ll not only lower your bills by five to 15 percent, but you will also extend the life of your entire A/C system. If you don’t change those clogged filters, it could create a malfunction, and you’ll have to get your unit repaired.

Turn Up Your Thermostat

Set it to 78 degrees and shed a few layers. Yes, this might not be preferable to your icy 72 degrees, but you know what will feel good? Seeing your electricity bill go down 18 percent.

Run the Ceiling Fan

This works in tandem with turning your thermostat to 78 degrees. If you’ve been running your fan clockwise during the previous months, be sure to change the direction so the air moves down into the room.

Invest In a Smart Thermostat

With these babies, you can regulate the temps when you’re not home from an app on your phone or via voice commands. For instance, you can set the A/C to a toasty 80 degrees when you’re not home to save money. Two good brands to check into are Nest and Ecobee. They’re well worth the cost.

Close Your Curtains and Blinds

When the sun’s rays enter your home, they heat up the room and your thermostat. The best time to shut your curtains and blinds is during the warmest part of the day, between (roughly) 10 a.m. and 3 p.m. This will help insulate your windows and stop the cool air from escaping.

Consider the Placement of Your Thermostat

Where do you have this? If it’s next to a hot window, your poor A/C will work harder than it needs to because it will think the room’s hotter than it is. Other places not to put it are near doors that could let in drafts. Or by bathrooms that are usually warm and steamy. In fact, the U.S. Office of Energy Efficiency and Renewable Energy advises avoiding placing thermostats near lamps or TVs. Why? They release heat that could confuse the sensors of your poor, struggling device.

Avoid Activities that Heat Up the House

Avoid using the oven, dishwasher, or dryer during the middle of the day. This heats up the house. Instead, use the microwave, grill outside, or wash your dishes by hand if you can stand it. If you need to dry clothes, wait until after sundown.

Check Your Air-Conditioner

If you had some issues with it last summer, get someone (a professional) to take a look at it before the high temps descend upon you. If you make a few small repairs, you’ll save mightily in the long run.

If you implement one or all of these tips, you’ll be in a much better, cooler place come full-on summer, the time of year when you most want to chill.

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

Thanks to the Great Resignation trend over the past year, there is a high availability of jobs. Therefore, now is a good time for retirees who would like to go back to work to ease into the job market. However, if you’ve already begun drawing Social Security benefits, you should understand how earning income will affect those payouts.

First of all, you have two options if you’d like to stop receiving Social Security. One option is available only if you’ve been drawing benefits for a year or less. In this case, you may cancel your application; but be aware that you must repay all the benefits that you and your family have received to date. That includes spousal benefits and even Medicare premiums that were deducted from your payout. You will still be able to reapply for Social Security later.

The second option is available only if you have reached full retirement age but have not yet turned 70 years old. In this case, you may request to have your Social Security payouts suspended.

There are two benefits associated with these strategies: 1) foregoing Social Security income will likely reduce your tax bill; and 2) your Social Security benefits will start accruing again based on the delay and calculations that include your new wages.

However, you may continue receiving Social Security while you work, which could be important if your spouse is receiving benefits based on your earnings record. Under this scenario, a portion of your benefit may be withheld or even subject to higher taxes. It all depends on how much you earn. If your annual income is $19,560 or less (2022), it won’t impact your Social Security benefits.

Note that only wages from a job or self-employment count toward your Social Security income limit for withholding purposes. Distributions you receive from pensions, annuities, investment income, interest, veterans benefits or other government or military retirement benefits are not considered earned income.

Once your income totals more than $19,560, the impact depends on your age. If you have not yet reached “full retirement age,” Social Security will withhold $1 in benefits for every $2 you earn over the limit.

During the year you reach full retirement age, your annual total earnings limit increases to $51,960 (2022), and the subsequent benefit reduction drops to $1 for every $3 you earn over that amount. In fact, they count only how much you’ve earned up to the month before your birthday – not what you end up earning in a whole year. Once you’ve reached full retirement age, it doesn’t matter much how you earn, there will no longer be any withholding of benefits.

Better yet, starting in January of the year after you turn full retirement age, regardless of whether you continue working or not, your Social Security benefit will increase to reflect any previously withheld benefits due to your income exceeding the limit. And if the years you subsequently worked rank among your 35 highest earning years, your payout will increase even more to reflect a higher benefit calculation (since you paid FICA taxes on that income).

Tax Considerations

In the case of all beneficiaries, at least 15 percent of Social Security income is exempt from federal income taxes. Be aware though, that for tax purposes, your reportable income includes half of your Social Security benefit plus all other forms of income, such as a job, pension or investment income. If your total annual income is between $25,000 and $34,000, then as much as 50 percent of your Social Security benefit is taxable. If you earn more than $34,000 in a year, then up to 85 percent of your Social Security benefit is subject to taxes.

This is a general overview of what happens to your Social Security benefits when mixed with earned income. There are additional details, so it’s a good idea to work with a Social Security expert to decide if you should cancel or suspend payouts, and to understand how your income and tax situation may be impacted by going back to work.

With that said, if your portfolio has taken a beating this year, you might want to stop investment distributions for now and give it time to grow. Fortunately, the United States is currently enjoying a robust job market in which highly experienced candidates can negotiate a flexible work schedule, job site and higher salary, so it may be worth it to go back to work for another year or two to help secure your long-term retirement plans.

How Social Security Benefits Are Affected by Earned Income

June 1, 2022 · Blog, Financial Planning

⏱ 4 min read

Thanks to the Great Resignation trend over the past year, there is a high availability of jobs. Therefore, now is a good time for retirees who would like to go back to work to ease into the job market. However, if you’ve already begun drawing Social Security benefits, you should understand how earning income will affect those payouts.

First of all, you have two options if you’d like to stop receiving Social Security. One option is available only if you’ve been drawing benefits for a year or less. In this case, you may cancel your application; but be aware that you must repay all the benefits that you and your family have received to date. That includes spousal benefits and even Medicare premiums that were deducted from your payout. You will still be able to reapply for Social Security later.

The second option is available only if you have reached full retirement age but have not yet turned 70 years old. In this case, you may request to have your Social Security payouts suspended.

There are two benefits associated with these strategies: 1) foregoing Social Security income will likely reduce your tax bill; and 2) your Social Security benefits will start accruing again based on the delay and calculations that include your new wages.

However, you may continue receiving Social Security while you work, which could be important if your spouse is receiving benefits based on your earnings record. Under this scenario, a portion of your benefit may be withheld or even subject to higher taxes. It all depends on how much you earn. If your annual income is $19,560 or less (2022), it won’t impact your Social Security benefits.

Note that only wages from a job or self-employment count toward your Social Security income limit for withholding purposes. Distributions you receive from pensions, annuities, investment income, interest, veterans benefits or other government or military retirement benefits are not considered earned income.

Once your income totals more than $19,560, the impact depends on your age. If you have not yet reached “full retirement age,” Social Security will withhold $1 in benefits for every $2 you earn over the limit.

During the year you reach full retirement age, your annual total earnings limit increases to $51,960 (2022), and the subsequent benefit reduction drops to $1 for every $3 you earn over that amount. In fact, they count only how much you’ve earned up to the month before your birthday – not what you end up earning in a whole year. Once you’ve reached full retirement age, it doesn’t matter much how you earn, there will no longer be any withholding of benefits.

Better yet, starting in January of the year after you turn full retirement age, regardless of whether you continue working or not, your Social Security benefit will increase to reflect any previously withheld benefits due to your income exceeding the limit. And if the years you subsequently worked rank among your 35 highest earning years, your payout will increase even more to reflect a higher benefit calculation (since you paid FICA taxes on that income).

Tax Considerations

In the case of all beneficiaries, at least 15 percent of Social Security income is exempt from federal income taxes. Be aware though, that for tax purposes, your reportable income includes half of your Social Security benefit plus all other forms of income, such as a job, pension or investment income. If your total annual income is between $25,000 and $34,000, then as much as 50 percent of your Social Security benefit is taxable. If you earn more than $34,000 in a year, then up to 85 percent of your Social Security benefit is subject to taxes.

This is a general overview of what happens to your Social Security benefits when mixed with earned income. There are additional details, so it’s a good idea to work with a Social Security expert to decide if you should cancel or suspend payouts, and to understand how your income and tax situation may be impacted by going back to work.

With that said, if your portfolio has taken a beating this year, you might want to stop investment distributions for now and give it time to grow. Fortunately, the United States is currently enjoying a robust job market in which highly experienced candidates can negotiate a flexible work schedule, job site and higher salary, so it may be worth it to go back to work for another year or two to help secure your long-term retirement plans.

Disclaimer

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

The Cash Conversion Cycle, also known as the Net Operating Cycle, answers the question, “How many days does it take a company to pay for and generate cash from the sales of its inventory?” However, before an analysis like this can take place, it’s important to consider the company’s primary line of business.

If the company sells software, it’s more challenging to measure performance if it generates revenue primarily on intellectual property – by developing computer code and licensing its use to clients. For online marketplaces, especially those that make the majority of their profits from third-party sellers that manage product sourcing, listing their inventory and shipping products on their own won’t measure the online marketplace’s own inventory. Since these types of businesses don’t act like a manufacturer that produces and sells products to other businesses or the general public, this type of analysis will be less helpful.

To start with the formula for the Cash Conversion Cycle (CCC), it’s calculated as follows:

CCC = Days of Sales Outstanding (DSO) + Days of Inventory Outstanding (DIO) – Days of Payables Outstanding (DPO)

Days of Sales Outstanding, Defined

DSO is the average number of days it takes a company to collect payment once a sale has completed. The beginning and ending Accounts Receivable figures from a fiscal year are added together and divided by 2. Then revenue from the income statement for the entire fiscal year must be divided by 365 days to get a daily average.

The fewer the days, the better; however, it can’t be so fast that such tight payment terms push customers away.

Days of Inventory Outstanding, Defined

DIO is the average number of days a business keeps its inventory before it’s purchased.

The beginning and ending inventories of a fiscal year are added together and divided by 2 to find an average. The resulting figure is then divided by the daily average of the cost of goods sold over a fiscal year, which is often 365 days.

DIO = Beginning Inventory + Ending Inventory / 2 = Cost of Goods Sold / 365 days

The lower the number, the faster inventory is sold. While there’s nothing wrong with moving it fast, there is the danger that orders might not be able to be fulfilled.

Defining the Operating Cycle

As the CFA Institute explains, putting DIO and DSO together constitutes the Operating Cycle. This is defined as the period of days that it takes a business to transform basic materials and/or goods into stock and obtain money from the completed transaction. When this number is small, it means product is moving and customers have no issue making prompt payments.

Days of Payable Outstanding, Defined

Days of Payable Outstanding determines the number of days a business takes to fulfill its debts to suppliers.

DPO = Beginning Accounts Payable + Ending Accounts Payable / 2 = Cost of Goods Sold / 365 days

Considerations for DPO include finding a balance between how long a business can take to pay their suppliers, but also not missing out on pre-payment discounts or being penalized with late fees, financing charges, etc.

Going Beyond the Results

When analyzing the Cash Conversion Cycle for the right type of company, it can provide great insight into a company’s efficiency in collecting billings; how long inventory is up for sale; and the time it takes to become current with its own suppliers. Depending on the results of the CCC analysis, performing financial analyses can provide insight into not only how the company is performing financially, but why the company is performing financially.

The Cash Conversion Cycle, also known as the Net Operating Cycle, answers the question, “How many days does it take a company to pay for and generate cash from the sales of its inventory?” However, before an analysis like this can take place, it’s important to consider the company’s primary line of business.

If the company sells software, it’s more challenging to measure performance if it generates revenue primarily on intellectual property – by developing computer code and licensing its use to clients. For online marketplaces, especially those that make the majority of their profits from third-party sellers that manage product sourcing, listing their inventory and shipping products on their own won’t measure the online marketplace’s own inventory. Since these types of businesses don’t act like a manufacturer that produces and sells products to other businesses or the general public, this type of analysis will be less helpful.

To start with the formula for the Cash Conversion Cycle (CCC), it’s calculated as follows:

CCC = Days of Sales Outstanding (DSO) + Days of Inventory Outstanding (DIO) – Days of Payables Outstanding (DPO)

Days of Sales Outstanding, Defined

DSO is the average number of days it takes a company to collect payment once a sale has completed. The beginning and ending Accounts Receivable figures from a fiscal year are added together and divided by 2. Then revenue from the income statement for the entire fiscal year must be divided by 365 days to get a daily average.

The fewer the days, the better; however, it can’t be so fast that such tight payment terms push customers away.

Days of Inventory Outstanding, Defined

DIO is the average number of days a business keeps its inventory before it’s purchased.

The beginning and ending inventories of a fiscal year are added together and divided by 2 to find an average. The resulting figure is then divided by the daily average of the cost of goods sold over a fiscal year, which is often 365 days.

DIO = Beginning Inventory + Ending Inventory / 2 = Cost of Goods Sold / 365 days

The lower the number, the faster inventory is sold. While there’s nothing wrong with moving it fast, there is the danger that orders might not be able to be fulfilled.

Defining the Operating Cycle

As the CFA Institute explains, putting DIO and DSO together constitutes the Operating Cycle. This is defined as the period of days that it takes a business to transform basic materials and/or goods into stock and obtain money from the completed transaction. When this number is small, it means product is moving and customers have no issue making prompt payments.

Days of Payable Outstanding, Defined

Days of Payable Outstanding determines the number of days a business takes to fulfill its debts to suppliers.

DPO = Beginning Accounts Payable + Ending Accounts Payable / 2 = Cost of Goods Sold / 365 days

Considerations for DPO include finding a balance between how long a business can take to pay their suppliers, but also not missing out on pre-payment discounts or being penalized with late fees, financing charges, etc.

Going Beyond the Results

When analyzing the Cash Conversion Cycle for the right type of company, it can provide great insight into a company’s efficiency in collecting billings; how long inventory is up for sale; and the time it takes to become current with its own suppliers. Depending on the results of the CCC analysis, performing financial analyses can provide insight into not only how the company is performing financially, but why the company is performing financially.

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

COVID-19 impacted the economy dramatically and commercial real estate was no exception in terms of decreased values. Often, the real property could no longer service the debt used to finance it. This debt restructuring and resulting debt forgiveness can result in taxable income.

Taxable Income and Debt Cancellation

If you have a $80,000 loan and the bank reduced the amount you owe down to $50,000, then you have an economic benefit of $30,000, which should be treated as taxable income. This is indeed how cancellation of debt is treated, but there are exceptions such as in the case of bankruptcy or insolvency. There is another unique scenario that applies only to commercial real estate.

Assuming that the taxpayer is not a C-corporation, debt cancellation is excludable from taxable income if it results from qualified real property business indebtedness (QRPBI). QRPBI is debt taken on to buy real property used for commercial purposes. Starting in 1993, debt used for building or improving a property also qualify.

As we all know, there is no such thing as a free lunch. In order for debt cancellation to not be considered current taxable income, the taxpayer must reduce their basis in the real property by this same amount. This does not cancel the income; instead, it defers its recognition and helps cash flow as a result. Below, we look at an example of how this works.

Illustrative Example

Assume David bought a property in 2017 and he uses it for business purposes. In 2022, the property has a first mortgage of $200,000 and a second mortgage of $100,000 (both with the same bank), with a fair market value (FMV) of $240,000. He negotiates with the bank to reduce the second mortgage down to $20,000, resulting in income from the cancellation of debt of $80,000.

The amount of debt cancellation that can be deferred is equal to the amount of the second mortgage before the debt cancellation, less the FMV minus the first mortgage. In David’s case, before debt cancellation, the FMV ($240k) minus the first mortgage ($200k) was $40,000. The balance of the second mortgage ($100k) exceeded this by $60,000. Out of the total debt cancellation of $80,000, this $60k is subject to deferral, with only the remaining $20,000 reported as immediate taxable income.

The $60,000 is not considered as taxable income only to the extent that David has sufficient adjusted tax basis in the depreciable real property to absorb this as a reduction in basis. Assuming this is the case, the reduction in basis applies the first day of the tax year after the debt cancellation (unless the property is sold before year-end – then it applies immediately).

In the example above, David would include the $10,000 of cancellation of debt income on his 2022 tax return and adjust his basis in the real property by $60,000 as of Jan. 1, 2023.

Filing Mechanics

For real estate held via partnerships instead of by individuals, determining if debt is QRPBI qualified happens at the entity level, although reductions of basis are done at the individual level for each partner, allowing individual planning. The election to defer cancellation of debt income is recorded on Form 982.

Conclusion

The COVID pandemic caused many real estate investors to restructure their debts. The option to defer debt income cancellation offers a great tax planning opportunity by delaying taxable income and improving cash flows.

Tax Break for Commercial Real Estate Investors

June 1, 2022 · Blog, Tax and Financial News

⏱ 3 min read

COVID-19 impacted the economy dramatically and commercial real estate was no exception in terms of decreased values. Often, the real property could no longer service the debt used to finance it. This debt restructuring and resulting debt forgiveness can result in taxable income.

Taxable Income and Debt Cancellation

If you have a $80,000 loan and the bank reduced the amount you owe down to $50,000, then you have an economic benefit of $30,000, which should be treated as taxable income. This is indeed how cancellation of debt is treated, but there are exceptions such as in the case of bankruptcy or insolvency. There is another unique scenario that applies only to commercial real estate.

Assuming that the taxpayer is not a C-corporation, debt cancellation is excludable from taxable income if it results from qualified real property business indebtedness (QRPBI). QRPBI is debt taken on to buy real property used for commercial purposes. Starting in 1993, debt used for building or improving a property also qualify.

As we all know, there is no such thing as a free lunch. In order for debt cancellation to not be considered current taxable income, the taxpayer must reduce their basis in the real property by this same amount. This does not cancel the income; instead, it defers its recognition and helps cash flow as a result. Below, we look at an example of how this works.

Illustrative Example

Assume David bought a property in 2017 and he uses it for business purposes. In 2022, the property has a first mortgage of $200,000 and a second mortgage of $100,000 (both with the same bank), with a fair market value (FMV) of $240,000. He negotiates with the bank to reduce the second mortgage down to $20,000, resulting in income from the cancellation of debt of $80,000.

The amount of debt cancellation that can be deferred is equal to the amount of the second mortgage before the debt cancellation, less the FMV minus the first mortgage. In David’s case, before debt cancellation, the FMV ($240k) minus the first mortgage ($200k) was $40,000. The balance of the second mortgage ($100k) exceeded this by $60,000. Out of the total debt cancellation of $80,000, this $60k is subject to deferral, with only the remaining $20,000 reported as immediate taxable income.

The $60,000 is not considered as taxable income only to the extent that David has sufficient adjusted tax basis in the depreciable real property to absorb this as a reduction in basis. Assuming this is the case, the reduction in basis applies the first day of the tax year after the debt cancellation (unless the property is sold before year-end – then it applies immediately).

In the example above, David would include the $10,000 of cancellation of debt income on his 2022 tax return and adjust his basis in the real property by $60,000 as of Jan. 1, 2023.

Filing Mechanics

For real estate held via partnerships instead of by individuals, determining if debt is QRPBI qualified happens at the entity level, although reductions of basis are done at the individual level for each partner, allowing individual planning. The election to defer cancellation of debt income is recorded on Form 982.

Conclusion

The COVID pandemic caused many real estate investors to restructure their debts. The option to defer debt income cancellation offers a great tax planning opportunity by delaying taxable income and improving cash flows.

Disclaimer

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

Suspending Normal Trade Relations with Russia and Belarus Act (HR 7108) – This legislation suspends normal trade relations with Russia and Belarus. The president may restore normal trade relations pending Congressional approval, and this authority is scheduled to end on the last day of 2023. The bill also permanently authorizes the president to impose visa- and property-blocking sanctions based on violations of human rights, as well as increase duty rates on products from these countries. These actions are designed to condemn Russia’s invasion of Ukraine by urging other World Trade Organization (WTO) members to suspend trade concessions to Russia and Belarus, and consider steps to suspend Russia’s participation in the WTO. The bill was introduced on March 17 by Rep. Richard Neal (D-MA). It passed in the House on the same day, passed in the Senate on April 7, and was signed into law by President Biden on March 17.

Modernizing Access to Our Public Land Act (HR 3113) – This bill was introduced by Rep. Blake Moore (R-UT) on May 11, 2021. It requires the Dept. of the Interior, the Forest Service, and the Corps of Engineers to digitize geographic information system mapping data relating to public access to Federal land and waters for outdoor recreation. This information, which must be made publicly available, will include status as to whether roads and trails are open or closed; the dates on which roads and trails are seasonally opened and closed; the types of vehicles allowed on each segment of roads and trails; the boundaries of areas where hunting or recreational shooting is regulated or closed; and the boundaries of any portion of a body of water that is closed to entry, watercraft or has horsepower limitations for watercraft. The bill passed in the House on March 15, the Senate on April 6, and is awaiting signature by the president.

Better Cybercrime Metrics Act (S 2629) – This bill authorizes various requirements to improve the collection of data related to cybercrime. For example, the Department of Justice must collect cybercrime reports from federal, state and local officials; include questions about cybercrime in the annual National Crime Victimization Survey; and evaluate current cybercrime data collection and reporting systems. The bill was introduced by Sen. Brian Schatz (D-HI) on Aug. 5, 2021. It passed in the Senate on Dec. 7, 2021, the House on March 29, and is awaiting the president’s signature to become law.

Bankruptcy Threshold Adjustment and Technical Corrections Act (S 3823) – The primary purpose of this legislation is to modify the eligibility requirements for a debtor to file for bankruptcy under Chapter 13. Specifically, only an individual (or an individual’s spouse, except a stockbroker or a commodity broker) with regular income that owes aggregated debt of less than $2,750,000 may file as a debtor under Chapter 13. The bill was introduced by Sen. Chuck Grassley (R-IA) on March 14 and passed in the Senate on April 7. It is currently under consideration in the House.

Countering Human Trafficking Act of 2021 (S 2991) – This bill authorizes the establishment of a Department of Homeland Security Center for Countering Human Trafficking. The goal is to address human trafficking with a victim-centered approach to increase the focus on and effectiveness of investigating and prosecuting forced labor cases. Specifically, the legislation centers on eradicating forced labor from both corporate and government agency supply chain contracts and procurement. The act was introduced by Sen. Gary Peters (D-MI) on Oct. 18, 2021. It passed in the Senate on April 16 and is under consideration in the House.

Ocean Shipping Reform Act of 2022 (S 3580) – This bipartisan act was introduced by Sen. Amy Klobuchar (D-MN) on Feb. 3. The bill increases the authority of the Federal Maritime Commission (FMC) to investigate late fees charged by common ocean carriers and otherwise find ways to promote the growth of U.S. exports through a more effective and economical ocean transportation system. For example, the bill prohibits common ocean carriers, marine terminal operators, and ocean transportation intermediaries from unreasonably refusing cargo space when available. This legislation passed in the Senate on March 31 and is under consideration in the House.

Restricting Trade Relations with Russia, Enhancing U.S. Export Pathways, and Bearing Down on Cybercrime and Human Trafficking

May 1, 2022 · Blog, Congress at Work

⏱ 4 min read

Suspending Normal Trade Relations with Russia and Belarus Act (HR 7108) – This legislation suspends normal trade relations with Russia and Belarus. The president may restore normal trade relations pending Congressional approval, and this authority is scheduled to end on the last day of 2023. The bill also permanently authorizes the president to impose visa- and property-blocking sanctions based on violations of human rights, as well as increase duty rates on products from these countries. These actions are designed to condemn Russia’s invasion of Ukraine by urging other World Trade Organization (WTO) members to suspend trade concessions to Russia and Belarus, and consider steps to suspend Russia’s participation in the WTO. The bill was introduced on March 17 by Rep. Richard Neal (D-MA). It passed in the House on the same day, passed in the Senate on April 7, and was signed into law by President Biden on March 17.

Modernizing Access to Our Public Land Act (HR 3113) – This bill was introduced by Rep. Blake Moore (R-UT) on May 11, 2021. It requires the Dept. of the Interior, the Forest Service, and the Corps of Engineers to digitize geographic information system mapping data relating to public access to Federal land and waters for outdoor recreation. This information, which must be made publicly available, will include status as to whether roads and trails are open or closed; the dates on which roads and trails are seasonally opened and closed; the types of vehicles allowed on each segment of roads and trails; the boundaries of areas where hunting or recreational shooting is regulated or closed; and the boundaries of any portion of a body of water that is closed to entry, watercraft or has horsepower limitations for watercraft. The bill passed in the House on March 15, the Senate on April 6, and is awaiting signature by the president.

Better Cybercrime Metrics Act (S 2629) – This bill authorizes various requirements to improve the collection of data related to cybercrime. For example, the Department of Justice must collect cybercrime reports from federal, state and local officials; include questions about cybercrime in the annual National Crime Victimization Survey; and evaluate current cybercrime data collection and reporting systems. The bill was introduced by Sen. Brian Schatz (D-HI) on Aug. 5, 2021. It passed in the Senate on Dec. 7, 2021, the House on March 29, and is awaiting the president’s signature to become law.